您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The US dollar index fell in the beginning of the week. The dollar extended its loss on Monday after US President Donald Trump decided to extend a March 1 deadline for additional tariffs on Chinese goods, suggesting progressive trade negotiations between the two countries. It rebounded from earlier lows on Thursday, after US data showed growth in the world's largest economy was stronger than expected in the fourth quarter. Both LME and SHFE base metals traded mixed over the week.

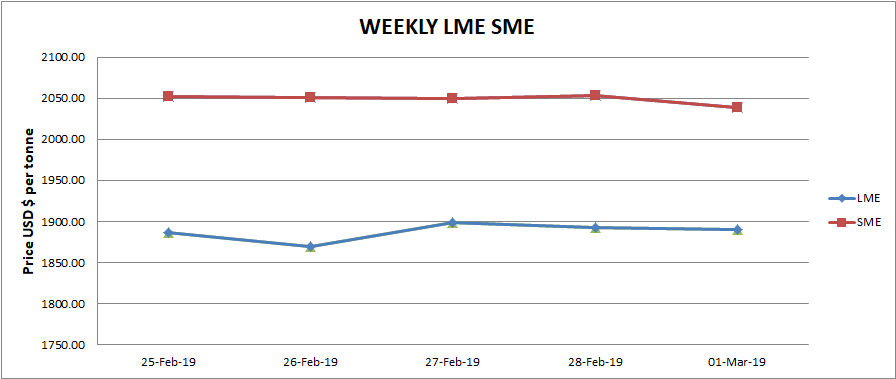

LME aluminium touched its highest on February 27 at US$ 1898.5 per tonne. News on full production recovery of Hydro’s Alunorte alumina refinery in Brazil buoyed the market. The prices then consolidated towards the end of the week and stood at US$ 1890.50 per tonne on Friday March 1. The contract is expected to trade within a tight range in the coming week.

{alcircleadd}

As on March 1, LME aluminium cash (bid) price stood at US$ 1890 per tonne, LME official settlement price stands at US$ 1890.50 per tonne; 3-months bid price stands at US$ 1910 per tonne, 3-months offer price is US$ 1910.50 per tonne; Dec 19 bid price stands at US$ 2043 per tonne, and Dec 19 offer price stands at US$ 2048 per tonne.

The LME aluminium opening stock decreased to 1232950 tonnes. Live Warrants totalled at 661725 tonnes, and Cancelled Warrants were 571225 tonnes.

LME aluminium 3-months Asian Reference Price is hovering at US$ 1911 per tonne.

The benchmark aluminium price on Shanghai Metal Exchange stayed almost flat over the week without much fluctuation. The price dropped to the lowest yesterday on Friday to US$ 2039 per tonne.

The SHFE 1905 contract fell below the five-day moving average, to a week low at RMB 13,610 per tonne in early trades yesterday. A buildup of longs buoyed it in the afternoon, and ended it at RMB 13,685 per tonne. Despite expectations of consumption boom in March-May, expanding inventories and falling prices of alumina will limit upward momentum in the coming week.

Responses