您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

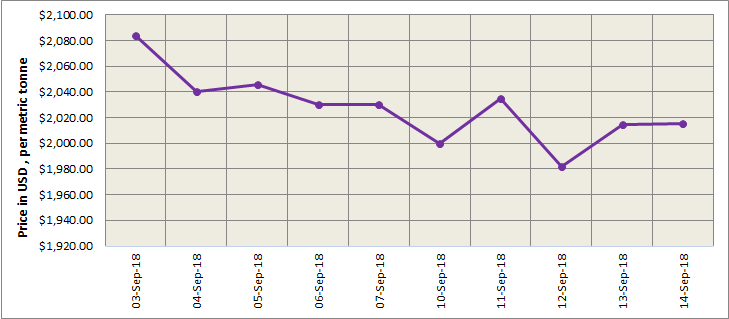

The first week of September was marked by a rising US dollar index and a falling LME aluminium graph. However, LME aluminium recovered during the second week. LME aluminium rose to a high of US$2,080 per tonne on September 10, after closing flat the previous week driven by the fact that workers extended their strike at Alcoa's alumina operations in Western Australia. The light aluminium contract traded within a range of US$ 2000 to US$ 2035 per tonne over the week.

Resumed NAFTA negotiations, falling US dollar, higher alumina prices, expectation around lifting of sanction on Rusal and sign of eased trade tension between China and the US are the factors that continued to drive the LME prices throughout the two weeks. The news that European consumers would avoid signing supply agreements with Rusal during Metal Bulletin’s 33rd International Aluminium Conference or the “mating season” for the aluminium industry in Berlin also had an effect on the prices.

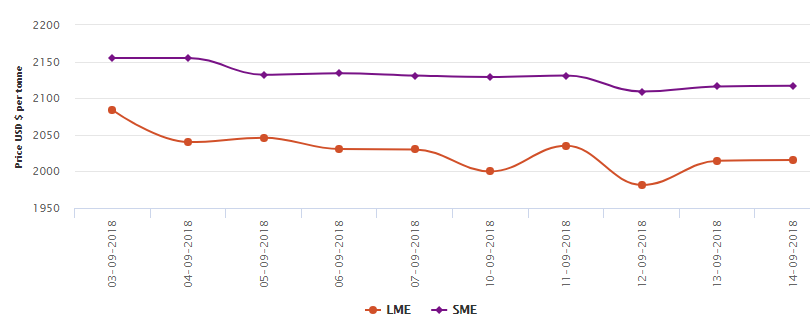

SME and SHFE Aluminium Prices registered a flat run through the first two weeks of September. Longs pulled the SHFE 1811 contract to a high and the contract closed at RMB 14,735 per tonne on September 10 with heavy pressure at the 20-day moving average. The Chinese market grew slow on weak downstream consumption and the news that China may ease aluminium production curbs in the upcoming heating season. However, the news of potential capacity cutbacks at Rusal will continue to bolster prices in the short run. The prices are expected to stay rangebound next week.

As on September 14, LME official settlement price stands at US$ 2015.5 per tonne; 3-months offer price is US$ 2054 per tonne and Dec 19 offer price stands at US$ 2090 per tonne. The LME aluminium opening stock stands at 1046700 tonnes.

The benchmark aluminium price on Shanghai Metal Exchange hovered within a narrow range of US$ 2109 per tonne and US$ 2131 per tonne over the week starting September 10.

A tight alumina market and higher prices continued to provide support to LME and SHFE aluminium. Alcoa’s and South32’s alumina refineries in Western Australia (WA) have delayed their shipments and workers continued their strike at Alcoa refinery plants and bauxite mines in WA. Meanwhile, maintenance at South32’s Worsley alumina refinery in WA affected output by some 200,000 tonnes. There is uncertainty around Rusal’s alumina supply to the market as sanctions are still in place. All these factors put pressure on the alumina market and the cost support will prevent downward room for aluminium prices.

Responses