您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

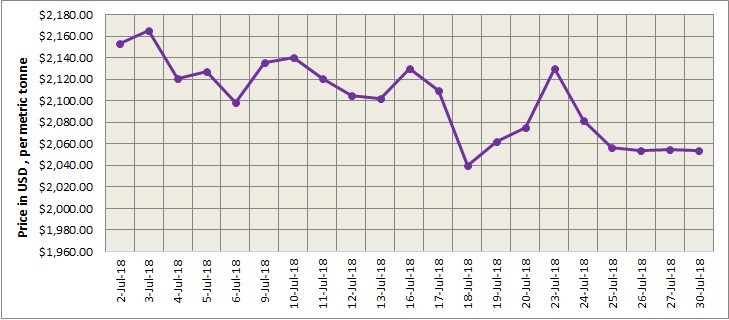

The US dollar index dipped 0.33% overnight and stood at 94.3, ahead of economic data release and central bank monetary policy meetings this week. LME base metals, except for zinc, rose across the board on Monday. After closing at US$ 2054 per tonne on Monday, LME aluminium climbed past the five-day moving average and hit a high of US$2,093 per tonne overnight. It is likely to extend its gains if its SHFE counterpart continues to strengthen. Shanghai Metals Market expects it to trade at US$2,070-2,090 per tonne today.

As on July 30, LME aluminium cash (bid) price stands at US$ 2052 per tonne, LME official settlement price stands at US$ 2054 per tonne; 3-months bid price stands at US$ 2073 per tonne, 3-months offer price is US$ 2074 per tonne; Dec 19 bid price stands at US$ 2122 per tonne, and Dec 19 offer price stands at US$ 2127per tonne.

The LME aluminium opening stock dropped to 1198250 tonnes. Live Warrants totalled at 851700 tonnes, and Cancelled Warrants were 346550 tonne.

LME aluminium 3-months Asian Reference Price is hovering at US$ 2054.40 per tonne.

SME and SHFE Aluminium Price Trend

The benchmark aluminium price on Shanghai Metal Exchange increased slightly to US$ 2106 per tonne on July 31, from US$ 2090 per tonne on July 30.

With support from longs, the SHFE 1809 contract inched up to stood firm at the five- and 40-day moving average yesterday. There was pressure at RMB 14,450 per tonne. The SHFE 1809 contract extended its daytime gains and hit a high of RMB 14,495 per tonne overnight. As primary aluminium inventory in China continued to shrink, the contract is likely to rise and try to break RMB 14,500 per tonne level today. The contract’s trading range is seen at RMB 1,400-14,550 per tonne today with spot discounts at RMB 120-80 per tonne.

US exemptions on Russian aluminium giant Rusal and the development of the US dollar will be the key factors to move both LME and SME.

Other factors to monitor today will be China's official manufacturing purchasing managers’ index (PMI) for July, Eurozone gross domestic product (GDP) growth in the second quarter, CPI for July, unemployment rate in June, US personal consumption expenditures (PCE) price index in June.

Responses