您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

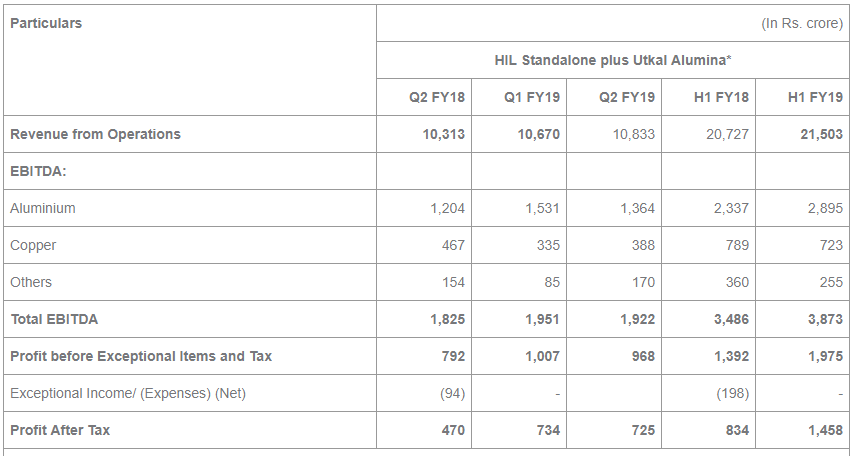

Hindalco Industries Limited, the metals flagship company of the Aditya Birla Group, announced Q2 FY19 results for Utkal Alumina, Hindalco standalone, as well as Aluminium Business. The company reported 5% increase in its Q2 FY2019 revenue at INR10,833 crore against INR10,313 crore in Q2 FY18. EBITDA (Earnings before Interest, Tax, Depreciation and Amortisation) at Rs.1,922 crore in Q2 FY19, compared to INR1825 crore in Q2 FY18. Net profit jumped 54% to INR 725 crore in Q2FY19 against INR470 crore in Q2FY18.

The performance rode on the back of supporting macros, improvement in operational efficiencies and better realisation. This was despite increase in input costs, mainly of coal and furnace oil.

{alcircleadd}

Revenue from its aluminium segment rose 18% to INR 6,135 crore, as compared to INR5,218 crore in Q2 FY18. EBITDA stood at INR1,364 crore in Q2 FY19, up 13 per cent compared to INR1,204 crore in Q2 FY18, on the back of supporting macros, partially offset by increase in the input prices.

The company has achieved consistent aluminium production of 326 thousand tonnes in Q2 FY19, as plants continued to operate at peak designed capacities.

Alumina (including Utkal Alumina) production was marginally lower at 701 thousand tonnes, from 712 thousand tonnes in the corresponding period last year due to operational issues on account of heavy rains during the quarter.

Aluminium Value Added Products (VAP, including Wire Rod) production was higher at 123 thousand tonnes in comparison to 119 thousand tonnes in Q2 FY18, regardless of the continuous surge in imports, which is a major challenge.

Responses