您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

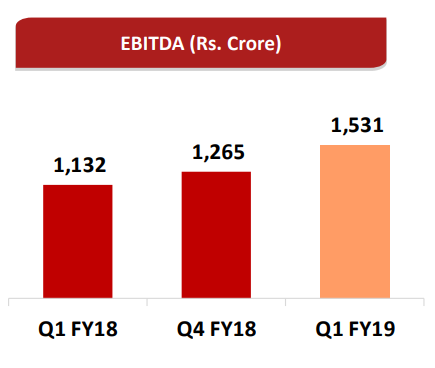

Hindalco reported Q1 FY19 results for Utkal Alumina, Hindalco standalone, as well as Aluminium Business. Though alumina production was marginally lower due to planned maintenance shutdown in one of the refineries, Hindalco reported an EBITDA of INR 1,531 crore (US$ 220 million) and a margin at 27 per cent, highest in the last 28 quarters, for Hindalco Aluminium Business including Utkal Alumina. EBITDA was up 35 per cent compared to INR 1,132 crore in Q1 FY18. The results also lifted the EBITDA for Hindalco standalone plus Utkal Alumina to INR1,951 crore, highest ever quarterly results for the group.

Hindalco’s aluminium revenue for Q1 FY19 stood at INR 5,667 crore. This increase was on account of better sales realisations and stable plant operations. The company achieved steady aluminium metal production of 323,000 tonnes in Q1 FY19, as its plants continued to operate at peak designed capacities.

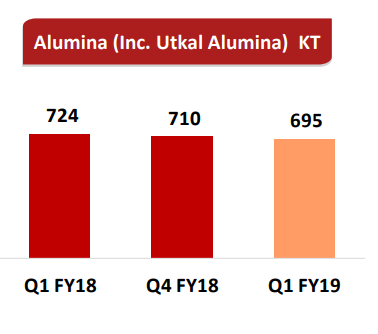

Alumina (including Utkal Alumina) production stood at 695,000 tonnes vs. 724,000 tonnes in the same period of FY18. Utkal Alumina’s brownfield capacity expansion of 500 kilo tonnes is on schedule and is expected to be completed by FY21.

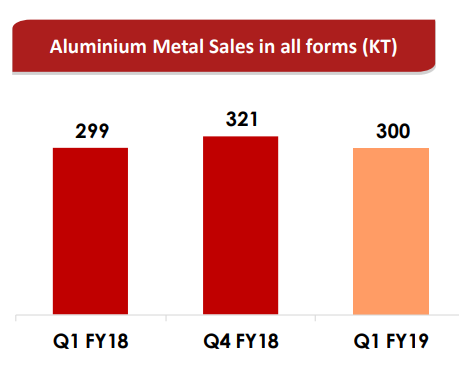

Aluminium Value Added Products (VAP, including wire rod) production was at 113,000 tonnes in comparison to 116,000 tonnes in Q1 FY18. The company managed to achieve sustainable production despite the influx of cheaper imports. Total aluminium sales volume for Q1 stood at 300,000 tonnes.

Hindalco Novelis’ revenues grew 16 per cent to US$3.1 billion, on the wings of higher average aluminium prices, higher shipments and better product mix. It achieved the highest ever quarterly adjusted EBITDA of US$332 million in Q1 FY19, up 15 per cent from Q1 FY18. Novelis’ net income was up 36 per cent YoY to US$137 million.

Novelis signed a definitive agreement to acquire Aleris Corp for value of US$2.58 billion in order to strengthen its leadership position in the automotive segment and it will mark its entry into the high-end aerospace segment.

Responses