您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

The Indian Carbon Credit Trading Scheme (CCTS) signifies India’s venture towards realising sustainability goals by reducing 45 per cent of greenhouse gas (GHG) emission intensity by 2030 compared to levels since 2005 and achieving net-zero by 2070. This groundwork was laid and implemented by the Energy Conservation (Amendment) Act, 2022, and the Detailed Procedure for Compliance Mechanism (BEE, 2023).

{alcircleadd}The independent Testing, Inspection and Certification Industry in India or the TIC Council India, has recommended implementation of the CCTS to foster a reliable and globally aligned market framework that lowers compliance pressures, maintains transparency, and strengthens India’s momentum toward achieving its climate commitments.

Explore the position of aluminium at the intersection of sustainability and strategy in Sustainability & Recycling: Aluminium's Dual Commitment

Impact of CBAM on Indian aluminium export

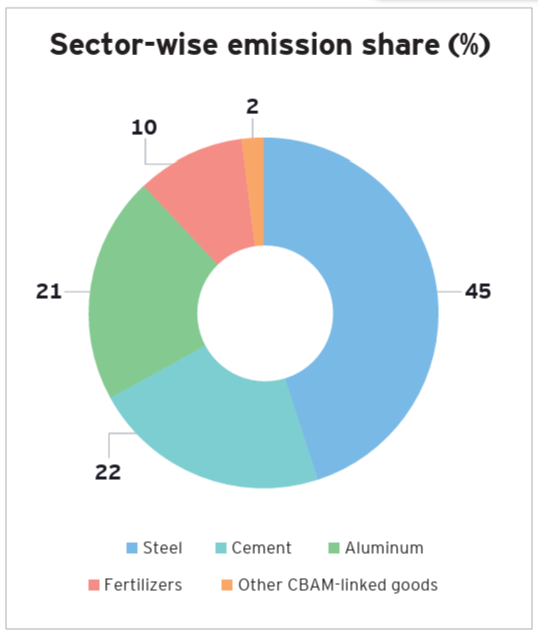

India ranked among the world’s most vulnerable economies to CBAM, with exports covered under the mechanism exceeding EUR 6 billion (USD 7.05 billion) to the EU, led primarily by iron and steel, followed by aluminium. The European Union’s (EU) Carbon Border Adjustment Mechanism (CBAM) imposes carbon-related compliance obligations on imports entering the EU.

In a report by the Indian Chamber of Commerce, CBAM was defined as a mechanism that “transforms carbon from a background compliance consideration into an explicit cost component of exports, with implications for price competitiveness, margins and contractual arrangements.”

The image has been sourced from "Carbon pricing meets raw materials: CBAM’s impact on Indian industries" by the Indian Chamber of Commerce

The report presented a breakdown of the percentage shares of embedded emissions across the sectors covered under the CBAM regulations.

27 per cent of Indian exports are shipped to the EU. Year-to-date till January 2025, India shipped 18,653.8 tonnes of unwrought aluminium to the EU market, which thereafter recorded a drastic drop in YTD January 2026, when the export volume of unwrought aluminium slipped to 10,874.72 tonnes, marking a staggering difference of 41.7 per cent. The declining rate in exports indicates the adverse effects left by CBAM implementation on the Indian export industry.

The Global Trade Research Initiative (GTRI) noted that several Indian exporters may have to reduce metal (aluminium and steel) prices by up to 15-22 per cent so that EU buyers absorb the carbon tax in their margins.

Worries among traders and exporters have intensified since the recommendations made by the European Parliament Committee on the Environment, Climate and Food Safety, that the scope of CBAM is being evaluated for further expansion. About 180 additional aluminium- and steel- based items could be included under CBAM starting January 1, 2028.

In an exclusive interview with AL Circle, Mr Alberto Monje Gama, Sustainability Policy Manager, TIC Council, regards the CBAM as more of a layered mechanism that is “complementary” to the EU’s Emissions Trading System.

“As free allowances under the EU ETS are gradually phased out and European producers face a stronger carbon price, there is a risk that production shifts to countries with lower or no carbon costs,” he explained. CBAM, therefore, “seeks to preserve a level playing field between EU manufacturers and global exporters,” pointing to the essentiality for foreign exporters like India to make note and take action.

To look for buying or selling leads of secondary aluminium ingot, visit our B2B marketplace.

Why should India opt for the CCTS?

CCTS is potentially a critical mechanism to assist the nation advance toward a low-carbon industrial economy while at the same time maintaining global trade competitiveness. The framework is designed in such a manner that it lays the foundation of a structured domestic carbon market that encourages industries to reduce GHG emissions through market-based incentives rather than relying solely on regulatory mandates.

The mechanism is especially important for energy-intensive sectors such as aluminium, power, cement, steel, fertilisers, refineries, and petrochemicals, whereby international trade is largely shaped by emissions monitoring and reporting. A strong and efficient Monitoring, Reporting and Verification (MRV) system is a key pillar of the mechanism, ensuring accurate GHG accounting and credibility of emissions data.

For India, the adoption of CCTS would usher in the following advantages:

Moreover, the regulation is aimed at lowering compliance burdens as it contributes to India’s accelerating progress toward national climate goals and net-zero ambitions.

How is the CCTS linked with the EU’s CBAM?

The CCTS is closely linked to CBAM, as it directly impacts carbon-intensive exports from countries like India, where 15 per cent of the total export volume is destined for the EU. Thus, India’s alignment with internationally accepted MRV and verification standards will become increasingly important for these export-oriented industries.

By implementing the CCTS, India can establish credible domestic carbon accounting systems, and exporters would be able to produce verified emissions data, thereby improving the nation’s compatibility with international carbon market standards.

For the aluminium sector, in particular, accurate emissions accounting is becoming essential because CBAM calculations increasingly examine embedded carbon emissions across the value chain.

Hence, implementing the CCTS in the Indian export framework to avoid paying heightened carbon tax at the EU borders becomes imperative. Gama, therefore, notes that “companies should prepare early to be better placed to maintain access to EU customers and differentiate themselves from competitors.”

TIC Council’s recommendations: How CCTS benefits the Indian export market

TIC Council India has proposed several recommendations to strengthen the effectiveness and credibility of the CCTS framework.

The council stresses that a reliable MRV framework is essential for ensuring transparency, integrity, and international acceptance of India’s carbon market. It recommends aligning India’s verification systems with internationally recognised frameworks such as ISO 14065, ISO 14066, ISO/IEC 17029 and UNFCCC accreditation principles.

For aluminium specifically, TIC recommends chemical or metallurgical engineering expertise, GHG accounting capability, ISO 14064 competency, as well as understanding of process-related emissions such as PFCs.

The council asserts that validation and verification agencies should operate as legally accountable entities capable of independent decision-making and contractual responsibility.

TIC Council also advocates for a globally credible framework that can minimise compliance burdens for Indian industries while safeguarding market integrity and export competitiveness.

Emphasising the need to identify the upside of the present circumstances, Mr Gama states, “CBAM also creates a strong incentive for Indian producers to improve emissions monitoring, invest in lower-carbon production, and strengthen their position in international markets where carbon performance is becoming increasingly important.”

To learn about the Indian Carbon Credit Trading Scheme in detail, download the TIC Council report.

Responses