您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The greenback recovered to 97 in the beginning of this week following its steepest weekly drop in three months last week. US President Donald Trump's upbeat comments on trade talks with China and Beijing's first major purchase of US soybeans in months have cut down on the trade war tensions.

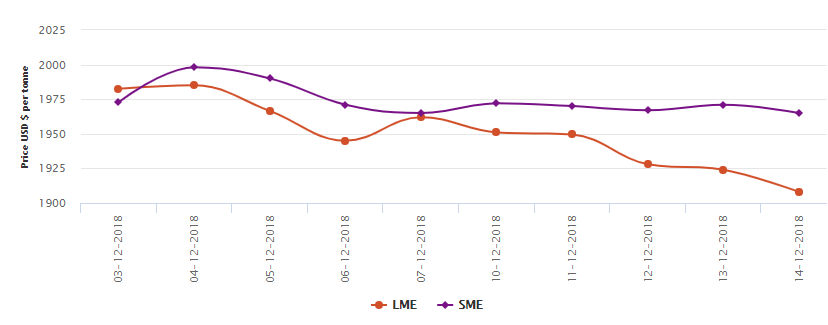

LME aluminium continued to trade weakly over the weak despite recovering some losses. The contract saw a trading range of US$ 1908- 1951 per tonne. Though the contract opened higher on Monday, it followed a steady downtrend with the strong US dollar and in absence of strong market fundamentals.

{alcircleadd}LME aluminium contract failed to stand firm above the 10-day moving average with resistance at the 20-day moving average. We expect it to remain weak in the coming week with most transactions within a range of US$1,910-1,940 per tonne.

As on December 14, Friday, LME aluminium cash (bid) price stood at US$ 1907per tonne, LME official settlement price stands at US$ 1908 per tonne; 3-months bid price stands at US$ 1920.50 per tonne, 3-months offer price is US$ 1921 per tonne; Dec 19 bid price stands at US$ 1977 per tonne, and Dec 19 offer price stands at US$ 1982 per tonne.

The LME aluminium opening stock increased to 1150100 tonnes. Live Warrants totalled at 909900 tonnes, and Cancelled Warrants were 240200 tonnes.

LME aluminium 3-months Asian Reference Price is hovering at US$ 1929 per tonne.

SME and SHFE Aluminium Price Trend

The benchmark aluminium price on Shanghai Metal Exchange followed a downward pattern over the week within a close range. The contract started the week at US$ 1972 per tonne and wrapped up the week’s trading at US$ 1965 per tonne.

The SHFE 1901 contract continued to trade weak and recovered some earlier losses to close at RMB13,615 per tonne on Friday. A weekly decline of 57,000 tonne in social stocks in China provided some support to SHFE aluminium prices. We expect the contract to trade at RMB13,600-13,750 per tonne in the coming week with spot discounts/premiums at RMB 20 per tonne. Decline in primary aluminium social inventories grew confidence across longs, against a backdrop of production cuts across domestic smelters. The contract is expected to test pressure at the five-day moving average.

Smelters in South China are struggling to turn to profit on slow demand and higher coal prices. Some smelters are announcing capacity cuts even without being ordered to do so, on environmental grounds. We see no significant upward room for LME and SHFE aluminium next week. The contracts will continue to trade lower under strong US dollar and low downstream consumption.

Responses