您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

On Thursday, February 2, China's aluminium billet inventories closed at 209,400 tonnes after recording a weekly surge of 42,200 or 25.3 per cent across five major consumption areas. In the first trading week following the CNY holiday in 2022 and 2021, the billet inventory had weekly gains of 25,000 tonnes and 18,000 tonnes, respectively. Most downstream businesses in east China restarted production, and recent transactions have been relatively busy. South China's output resumed quite slowly, which put much strain on inventories. Next week, it's anticipated that the social inventory will continue to rise but more slowly.

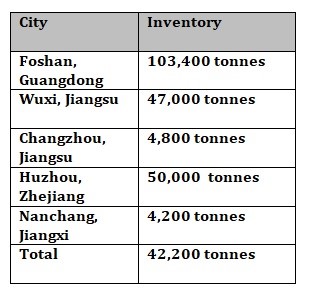

The figure below provides further information on the current state of aluminium billet inventories in China:

In particular, the inventory in Foshan hiked by 27,500 tonnes from January 28 to 103,400 tonnes, and the cargoes were primarily from the southwest of China. In contrast, most sources from the northwest of China, such as Xinjiang, were shipped to the east of China because the prices there were comparable. To reach 47,000 tonnes and 50,000 tonnes, respectively, Wuxi and Huzhou experienced growth of 4,200 tonnes and 8,000 tonnes.

On the same day, Changzhou and Nanchang's inventories climbed by 2,300 tonnes and 200 tonnes to score at 4,800 tonnes and 4,200 tonnes. In the first trading week following the CNY vacation, most downstream businesses in east China essentially restarted production and recent transactions were relatively busy. South China's output resumed quite slowly, which put much strain on inventories. Next week, it's anticipated that the social inventory will continue to rise but more slowly.

Responses