您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

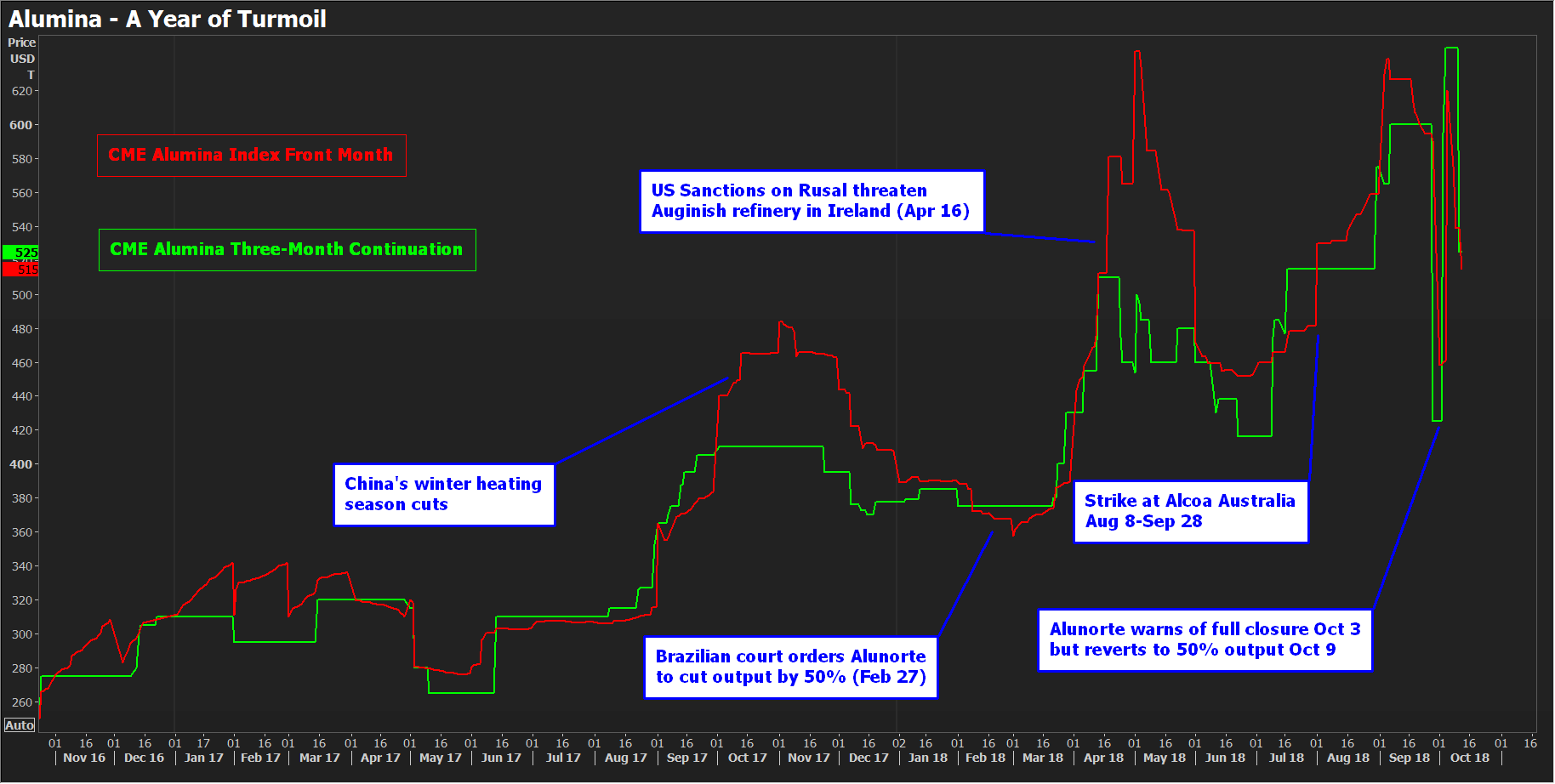

The alumina market is going through the most topsy-turvy and volatile period with sharp rise and fall in prices and supply disruptions. The temporary closure of Hydro’s Alunorte alumina refinery in Brazil and uncertainties surrounding U.S. sanction on Rusal pushed up alumina price sky high driving the export market. According to China Customs data, China's exports of alumina increased more than fivefold MoM in September to 166,000 tonnes, the highest monthly volume in 2018. The country's year-to-date exports of alumina exceeded imports for the first time this year. China imported 30,000 tonnes of alumina in September, customs data said. China has finalized orders for the rest of this year for at least 100,000 tonnes of alumina per month.

The monthly average spot price for domestic alumina surged RMB 185 per tonne (US$27/t) month on month to RMB 3302 per tonne (US$ 475.32/t) in September from RMB 3117 per tonne (US$ 449/t) in August. While the monthly average Australian alumina FOB price for September stood at US$ 602.05 per tonne. Such overwhelming prices drove alumina export from India, China and Vietnam in the first three quarters of CY 2018.

{alcircleadd}

Image: Reuters

According to Nalco, in Q2 CY 2018, the average price realisation for alumina was US$555 per tonne. It is quite high and in Q3 CY 2018, alumina prices stood at around US$550 per tonne. Nalco drives the alumina export segment in India every year being the top alumina producer and exporter. With the financial issues on track, Anrak alumina is expected to start operations in the third quarter of 2019 and add about 600,000 tonnes of alumina to India’s total capacity in H2 2019.

However, we are not certain how the market is going to turn in the fourth quarter of 2018. The federal environmental agency IBAMA lifted the embargo on Hydro Alunorte’s DRS 2 yesterday, after reviewing the information requested from Alunorte and SEMAS, the local environmental agency. This followed an authorization granted by IBAMA to utilize its state-of-the art press filter technology in processing of bauxite residues. However, Embargo on DRS2 from the federal court system remains in place. This works as a sustainable solution for Alunorte facilitating 50% current operations. This has generated positive sentiment in the market releasing supply concerns and opening up further avenues for restarting of full operations in the refinery.

According to sources, the Nalco’s recent tender for 30,000 tonnes of alumina went to EGA for US$488 per tonne. Vinacomin is expected to settle its mid-November bids at around US$435 per tonne. Industry analysts for bauxite and alumina forecasted an average API price of US$425 per tonne for 2019. This may go down if Alunorte comes on stream in full capacity by January 2019.

Alcoa will have about 300,000 tonnes of surplus alumina to sell next year as they closed 2 smelters in Spain. Unionised workers at Alcoa’s Western Australian operations agreed to end their strike in September end after signing a new wage agreement. On the other Rusal sanction deadlines have been extended to December 12.

The current Australian alumina FOB price stands at US$489 per tonne, down about 19 % from September prices of US$ 602 per tonne. The alumina prices are expected to be around US$ 450 to 480 per tonne in the last quarter of 2018. Forecasting alumina prices for the medium term continues to remain risky due to the volatility in the market. It remains to be seen how the key players wrap up their operational issues in the first quarter of 2019.

Responses