The global aluminium market in 2026 is not facing a typical cycle shift; it is undergoing a structural stress test. What began as a marginally tight market has rapidly evolved into a supply-risk-driven environment, where geopolitics, logistics and energy stability are now as critical as demand fundamentals.

This shift is best understood through the lens of China market analysis, European market research, consumer research report insights, and broader industry trend analysis, all of which point to a single conclusion: aluminium is no longer just a commodity; it is a strategic supply chain story.

We have recently updated our Global Aluminium Industry Outlook 2026, delivering deeper granularity into the near- to mid-term shifts shaping the global aluminium landscape.

A market already on edge, now amplified

The Gulf region, contributing roughly 8–8.8 per cent of global aluminium production (6-6.5 million tonnes), plays a disproportionately large role in global trade flows. With 5-5.5 million tonnes moving through the Strait of Hormuz, the region is not just a production hub; it is the backbone of tradable supply.

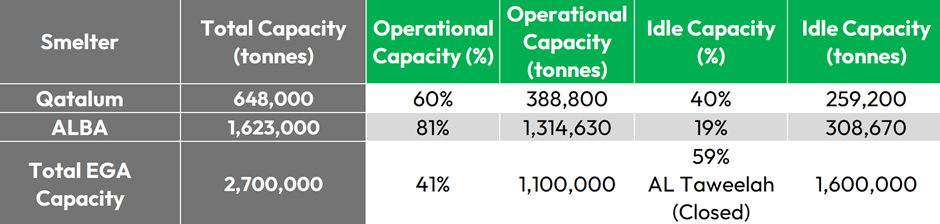

Status of GCC aluminium smelters

The current Middle East tensions have not created a new dynamic. Instead, they have intensified an already tight market, pushing it toward a supply-constrained, cost-push regime and this is not about demand destruction, It is about supply fragility.

The real risk: Logistics, not just production

Traditional market size analysis would focus on output losses. But today’s disruption is more complex.

- Production remains relatively resilient.

- Logistics and shipping routes have emerged as the weakest link.

- Energy-linked risks are compounding operational uncertainty.

The Strait of Hormuz has effectively become the single largest systemic risk to global aluminium flows. Even partial disruptions here can trigger cascading effects across Europe and Asia.

In this context, tracking smelter closures alone is insufficient. What matters now is real-time monitoring of logistics flows, energy inputs and operating rates, a far more dynamic approach than conventional forecasting.

From tightness to “Stress Deficit”

Entering 2026, the aluminium market was expected to be marginally tight. Today, it is transitioning into what can be described as a “stress deficit” scenario.

- Estimated primary aluminium deficit: 1.7-2.4 million tonnes

- Market condition: Structurally tight, with volatility spikes

- Pricing behaviour: Elevated premiums, intermittent shocks

The closure of the Mozal Aluminium Smelter (~0.57 million tonnes capacity) adds another layer of pressure, particularly for the European market research landscape, where dependency on imported metal remains high.

The result? A clear shift toward a seller’s market.

Demand is not immune

While supply constraints dominate headlines, consumer research report indicators show that demand is already reacting.

- European automotive sector: Subdued outlook

- U.S. auto sales: Declining trend

This is a critical nuance. The market is not collapsing, but demand is becoming cautious, delayed and selective.

In essence, aluminium is entering a phase where:

- Supply is constrained

- Costs are rising

- Demand is adjusting, not disappearing.

Opportunistic flows: The Russian factor

One of the most telling developments in recent industry trend research is the reemergence of Russian aluminium in global trade flows.

In a disrupted market:

- Demand becomes geographically redistributed.

- Trade becomes politically filtered.

- Pricing becomes discount-driven

A clear example is Japanese auto component manufacturers exploring procurement of Russian primary foundry alloys (PFA).

This is not a structural shift; it is opportunistic demand, driven by immediate supply gaps.

In an increasingly volatile environment, informed decision-making requires timely and actionable market intelligence. Let’s connect to explore how these insights can support your strategic priorities.

Voyagerman Technology

Voyagerman Technology

{kind=link}