The Middle East has long been a cornerstone of the global primary aluminium ecosystem. It is built on competitively priced energy and a strategic vision to diversify beyond hydrocarbons. Today, the region serves as an important backbone of the aluminium supply chain (excluding China).

But in times of geopolitical disruption, even the strongest pillars are being tested.

From a competitive analysis market research perspective, the current crisis in the Middle East is more than just a short-term disruption. It is now a structural stress test for global aluminium trade flows.

In this blog, we’ll break down what measures top aluminium companies in the Middle East are taking amidst geopolitical disruptions.

When disruption becomes market reality

Port closures, logistical bottlenecks, and production constraints are active market forces in the Middle East aluminium trade. Any sustained disruption in metal outflows from the GCC region could significantly tighten the global supply-demand balance over the next 6 to 12 months.

This comes at a time when the aluminium market is already leaning toward a structural deficit.

What makes the situation more critical is the absence of immediate alternatives. No other region today offers the same combination of scale, speed and reliability to replace Middle Eastern supply in the short to medium term. This imbalance is clearly reflected in emerging market statistics, indicating upward price pressure.

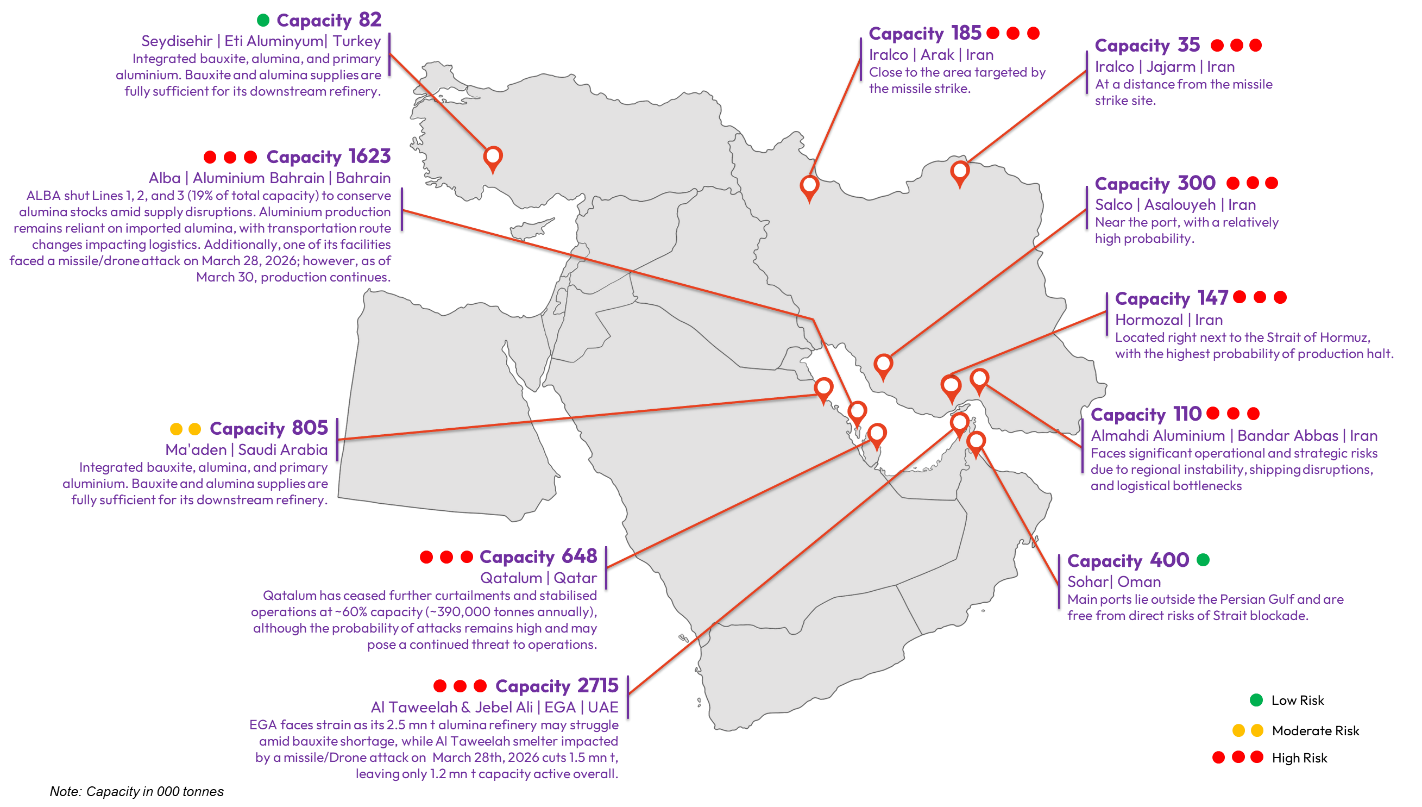

Middle-East aluminium smelters capacity & risk assesments

Source: AL Circle Research

Rising costs and shifting trade dynamics

The ongoing global crisis is reshaping the cost structures across the aluminium value chain. Increasing logistics complexity, higher insurance premiums and the need to diversify shipping routes are driving up raw material costs.

From a focus market lens, this is not just about transportation. It’s about margin erosion and operational resilience. Producers in the Middle East are now navigating a landscape where every logistical decision directly impacts net income and supply continuity.

Production pressures: A deeper look

Now let’s take a closer look at some regional operations highlighting the scale of this challenge:

- Qatalum is operating at approximately 60% capacity due to a reduced level of gas supply from Qatar Energy.

- Aluminium Bahrain (ALBA) is maintaining production at around 81% capacity utilisation, primarily through potlines 4, 5 and 6, to avoid shutdown risks.

These constraints are expected to widen the supply gap, with aluminium prices projected to range between USD 3,400 and USD 4,000/4200 per tonne.

Aluminium market balance (tonnes) & price scenarios (tonnes/USD)

Source: AL Circle Research

Such shifts are increasingly captured in consumer trends reports, where downstream industries are already preparing for price volatility and supply uncertainty.

Logistics innovation: The new competitive edge

ALBA’s strategic rerouting

In response to disruptions in the Strait of Hormuz, ALBA has demonstrated remarkable agility. They have rerouted 40% to 60% of their aluminium exports through Saudi Arabia’s Jeddah port. This involves an overland journey of approximately 1,400 km.

Despite force majeure conditions and production challenges:

- Transportation costs have remained broadly stable.

- Delivery timelines have been maintained.

ALBA currently holds around one month of alumina inventory and continues to rely on regional support, including additional supply from Ma’aden in Saudi Arabia.

This is a textbook case of how supply chains can be re-engineered under pressure, an insight often highlighted in advanced competitive analysis market research frameworks.

EGA’s Oman pivot

Similarly, Emirates Global Aluminium (EGA) has adapted by shifting its logistics through Oman’s Sohar port, ensuring both export continuity and raw material inflows.

This involves overland transportation between Sohar and UAE-based smelting facilities. It is a strategic move to bypass constraints in the Strait of Hormuz.

In news: Iranian strikes hit EGA and Alba’s aluminium smelters

What this means for the global market

The ongoing adjustments by major Middle East aluminium producers highlight a broader transformation:

- Supply chains are becoming more regionalised and flexible.

- Logistics is emerging as a key competitive differentiator.

- Risk management is now central to operational strategy.

From a market research standpoint, the crisis brings out a critical reality: resilience is now a defining factor of market leadership.

As the situation evolves, stakeholders across the aluminium value chain, from producers to end-users, will need to rely more heavily on market statistics, consumer trends reports and real-time intelligence to navigate uncertainty.

Final thought

The Middle East aluminium industry is not just reacting to disruption. It is redefining how global supply chains operate under pressure. And in doing so, it is setting new benchmarks for resilience, adaptability and strategic execution in an increasingly volatile world.

Make every decision count: Get in touch with us for deeper analysis and informed decision-making.

Voyagerman Technology

Voyagerman Technology

{kind=link}