您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

This report is a compilation of comprehensive strategic analysis of global red mud generation trends, future commercial utilisation pathways, critical mineral recovery opportunities, low-carbon construction material applications, environmental remediation potential and circular economy integration shaping the industry till 2036. The study provides long-term visibility into commercially scalable applications, future buyer industries, investment hotspots, refinery expansion impact, sustainability-driven industrial adoption trends and the evolving role of red mud as a strategic secondary resource across global industries.

Inside the global red mud transformation & commercial opportunity landscape

Aluminium does not occur naturally, although it is the most abundant metal in the earth’s crust. The common precursor to aluminium metal is alumina (aluminium oxide) and around 95% of the alumina produced today is derived from bauxite through the Bayer process. While aluminium offers a plethora of benefits, concerns remain with red mud (bauxite residue), a slurry by-product formed when alumina is produced from bauxite.

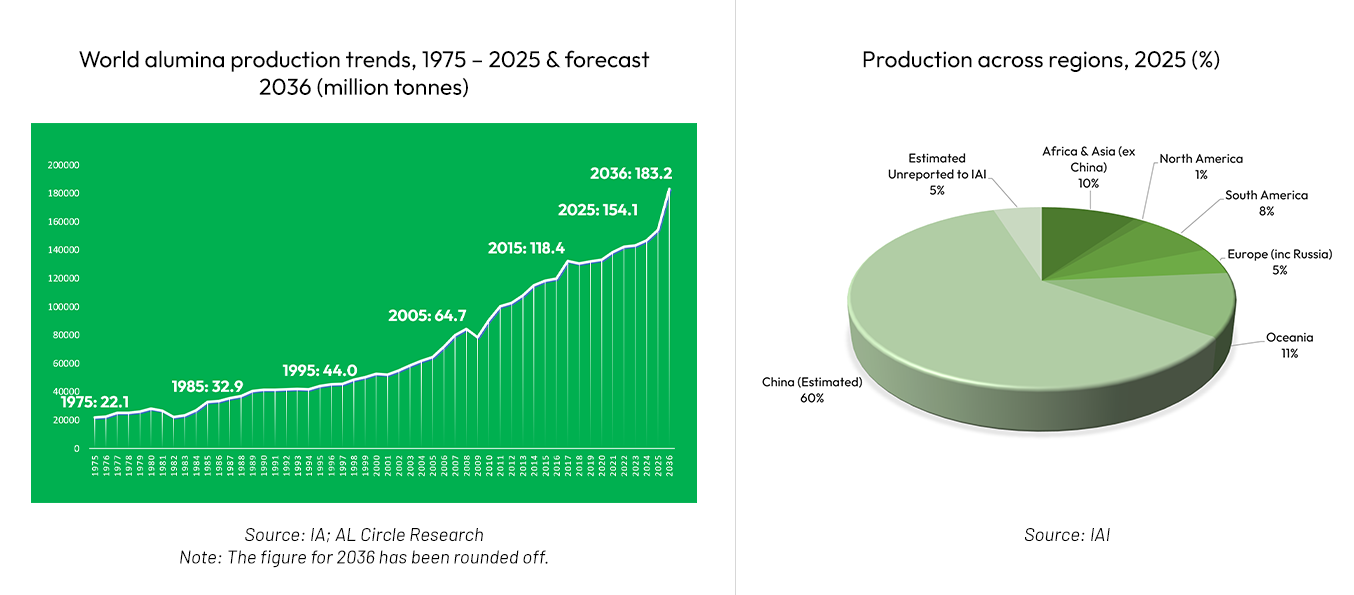

Alumina production worldwide stood at around 155 million tonnes in 2025. The key alumina-producing countries, including China, Australia, Brazil, and India, account for about 81%-83% of the global production.

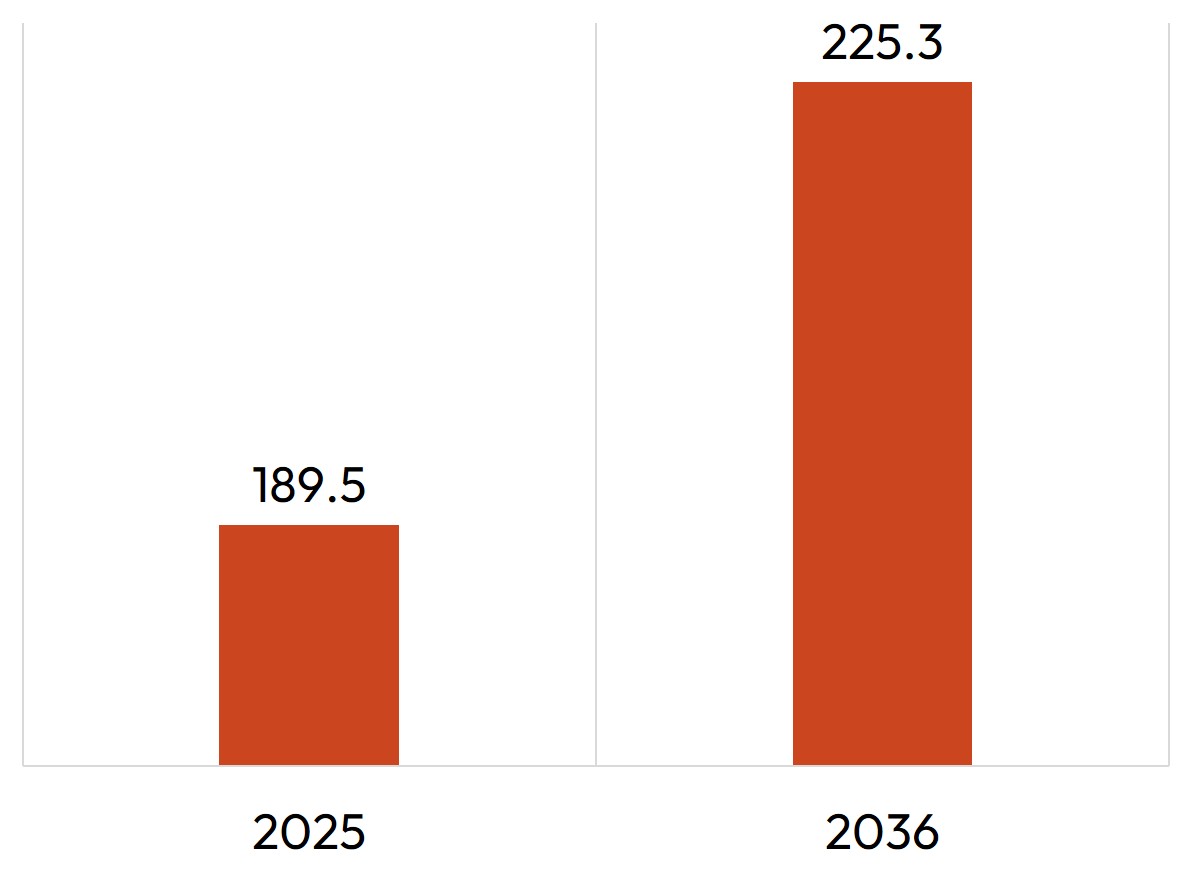

For every tonne of alumina produced globally, around 1.23 tonnes of red mud are generated on average. In 2025, alumina refineries worldwide are estimated to have generated nearly 189.5 million tonnes of red mud, highlighting the growing scale of residue management challenges across the aluminium value chain. And here’s not the end. By 2036, red mud production is estimated to reach a staggering volume of 225.3 million tonnes.

Global red mud generation snapshot, 2025 & forecast 2036

Source: AL Circle Research

Note: Red mud generation is a theoretical estimate based on various research studies on 1.23 tonnes of red mud generated for 1 tonne of alumina produced

Industry concerns surrounding red mud disposal and storage intensified significantly following the 2010 tailings dam failure at the Ajka alumina plant in Hungary, which resulted in severe flooding, casualties and large-scale environmental impact.

Although aluminium recycling may help reduce part of the pressure, sustained growth in primary aluminium demand is expected to continue driving alumina production in the foreseeable future, leading to higher red mud generation globally. Legacy and active tailing dams storing red mud therefore remain a critical operational, environmental and long-term sustainability challenge for the global aluminium industry.

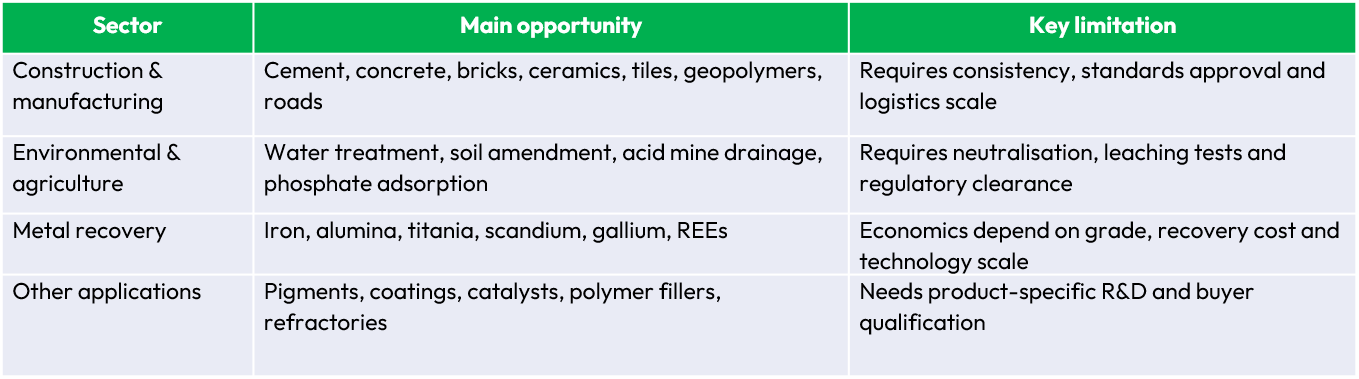

Where are the next commercial opportunities in red mud emerging

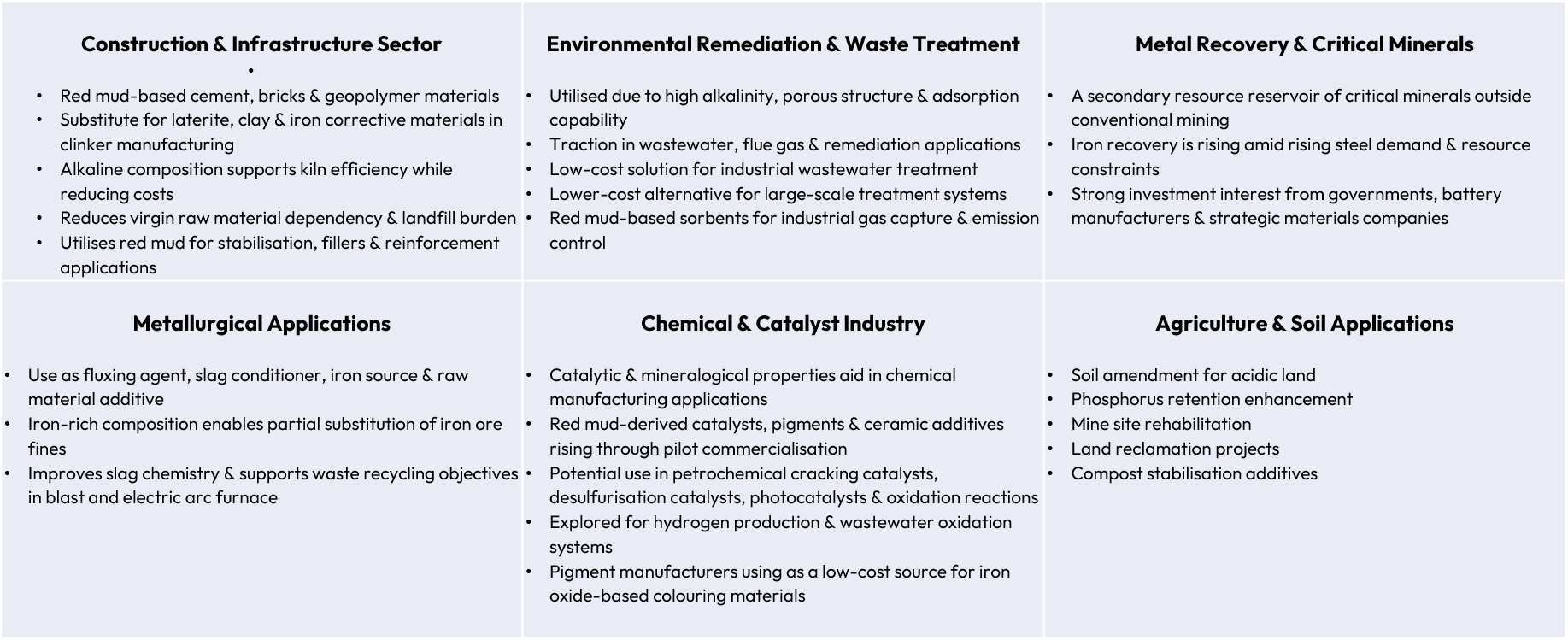

Red mud is increasingly evolving from a hazardous industrial waste into a strategic secondary resource with multi-sectoral potential. Growing environmental regulations, landfill restrictions, decarbonisation goals and circular economy initiatives are driving industries to explore red mud as an alternative raw material, adsorbent, mineral substitute and metal recovery feedstock.

Current utilisation trends show that the strongest commercial opportunities lie in construction materials, environmental remediation and metal recovery applications, while emerging opportunities are developing in advanced materials, carbon capture, catalysis and critical mineral extraction.

Red mud utilisation by sector

Source: Journal of Arab American University

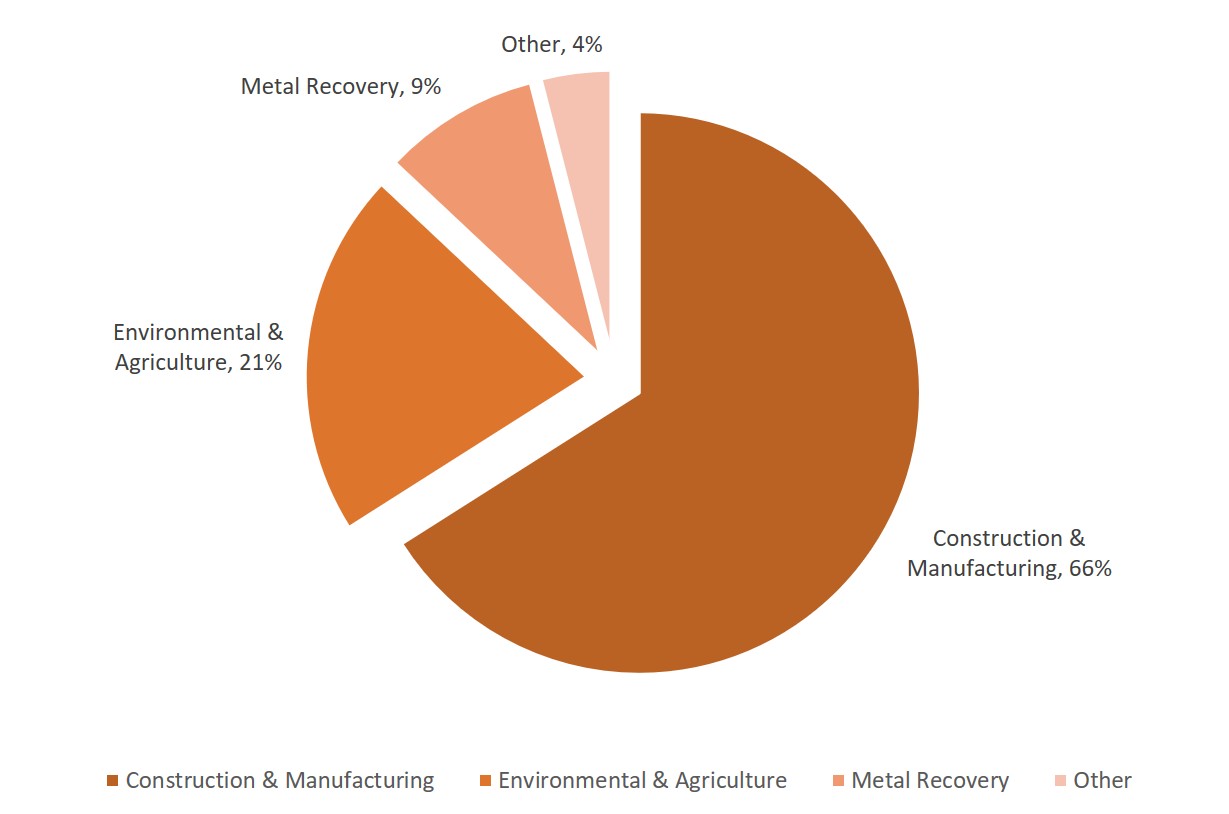

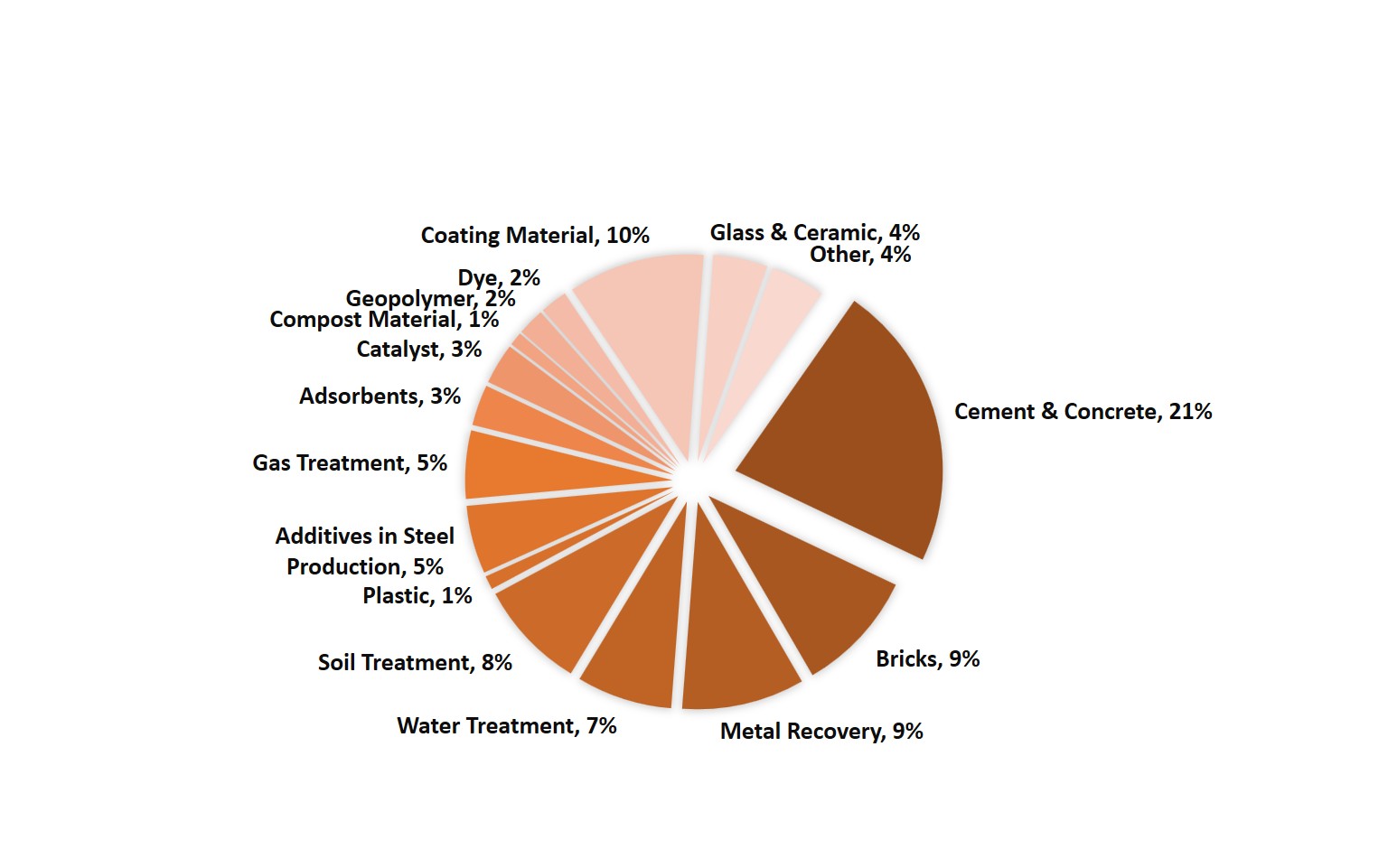

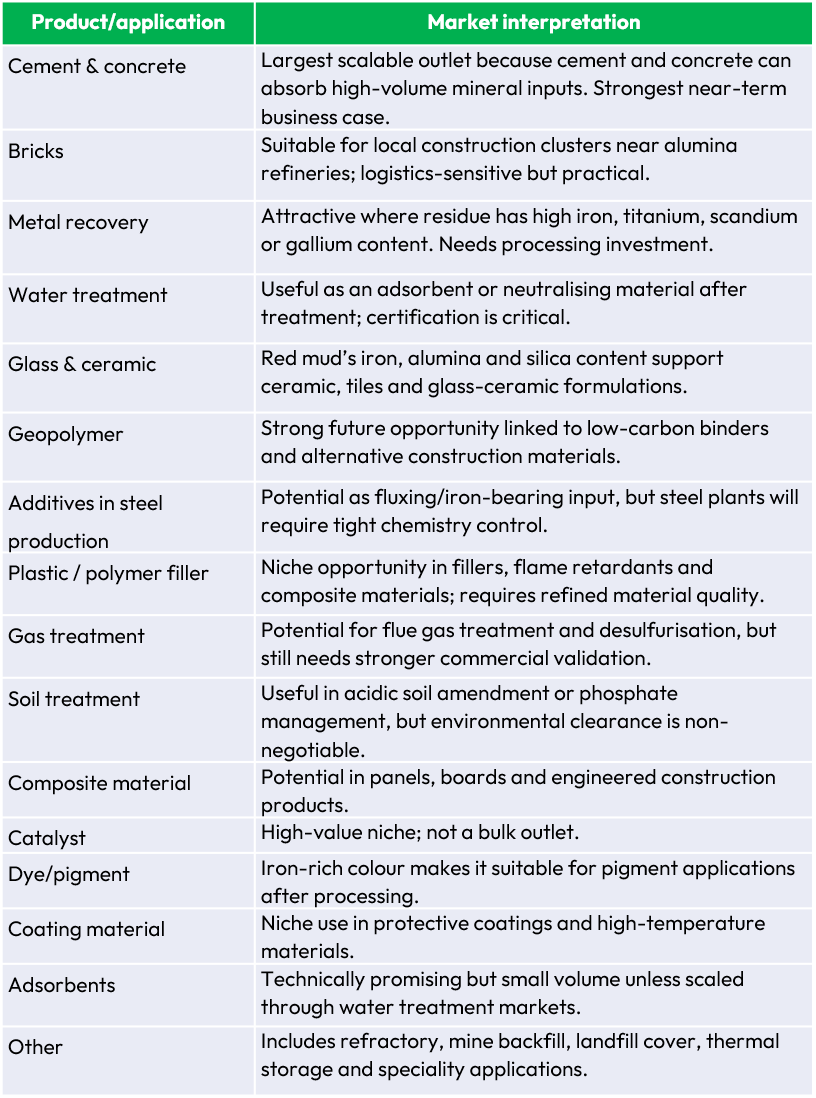

Red mud utilisation by product

Source: Journal of Arab American University

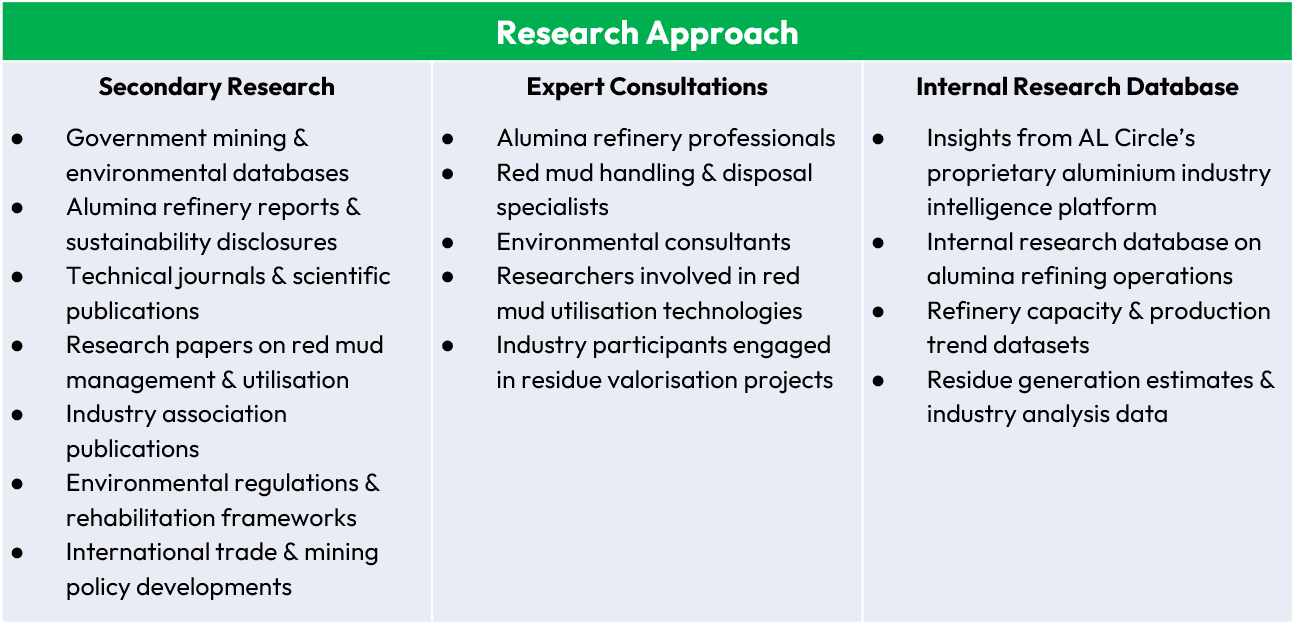

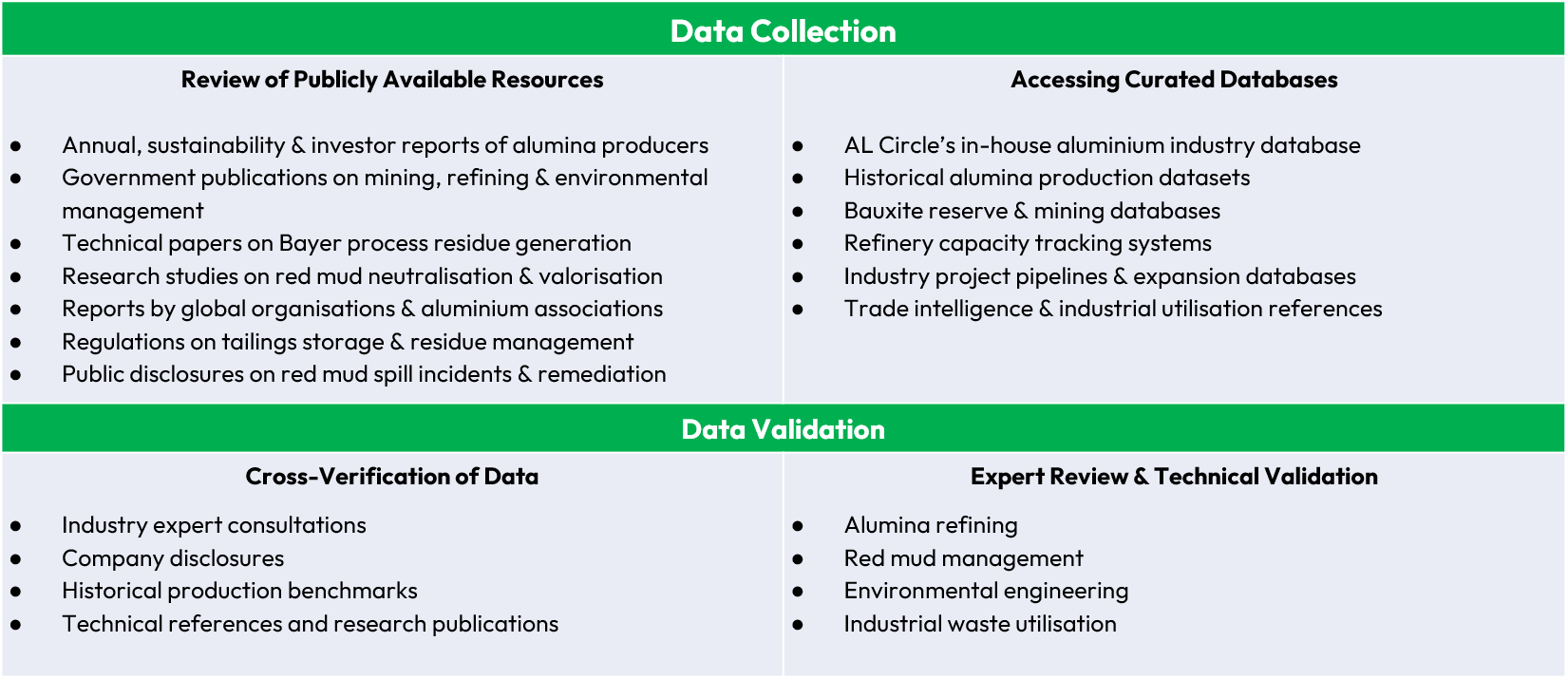

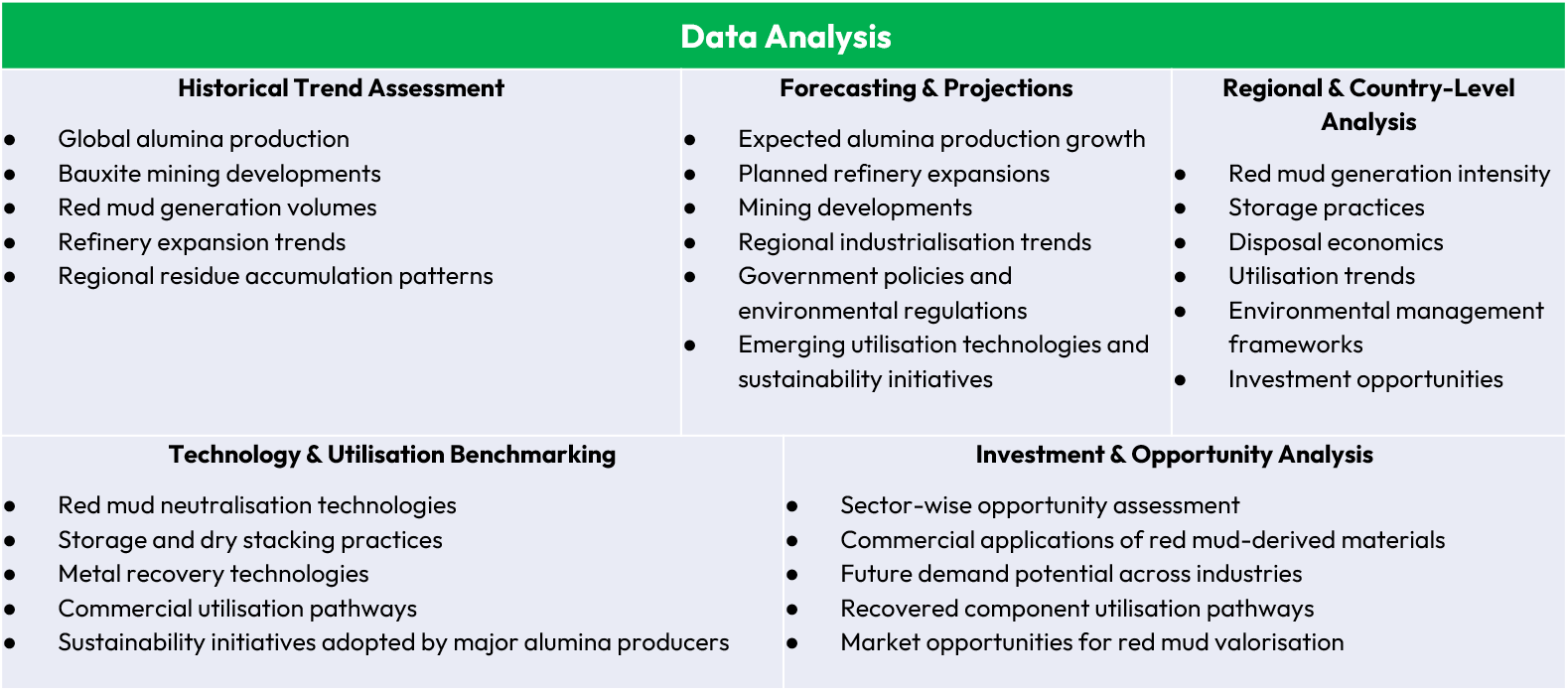

How this strategic industry assessment was developed

Our study on the Global Red Mud Industry adopts a comprehensive and structured research methodology to evaluate global red mud generation trends, storage practices, disposal economics, utilisation pathways, environmental concerns and emerging commercial opportunities associated with bauxite residue. The research was conducted through an integrated approach combining extensive secondary research, expert consultations, industrial benchmarking, and analytical modelling. The methodology framework is detailed below:

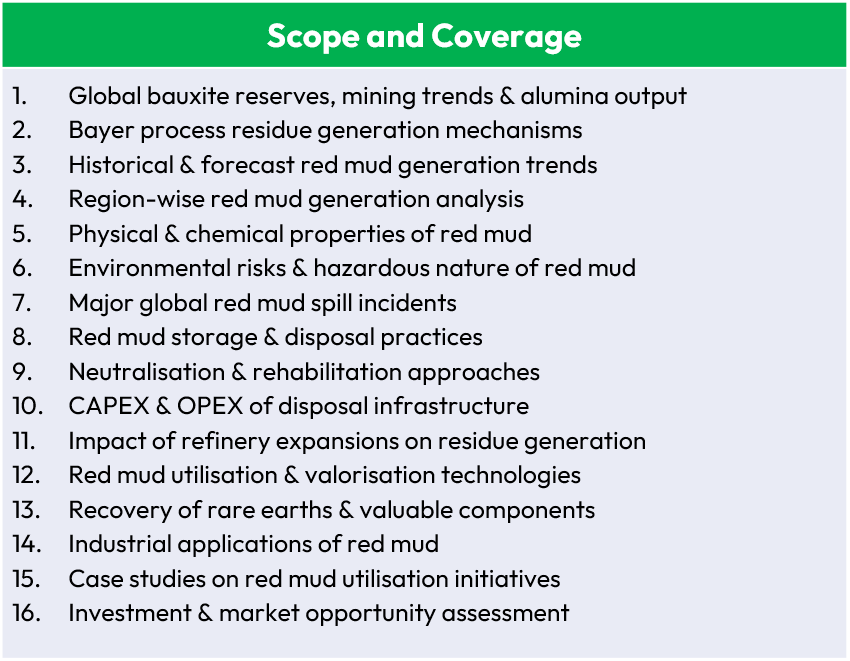

What will you understand from this strategic red mud industry report?

Frequently asked questions