Vedanta Resources Plc. releases the production report for the First Quarter ended 30 June 2016. Highlights from the aluminium section point towards a number of positives despite the volatile market and raw material insecurity, the company has been struggling with.

Operation highlights:

• Achieved production run-rate of 1.1mtpa

• Complete ramp-up of first line of 1.25mt Jharsuguda-II smelter , second line commenced in July;

• 325kt BALCO-II smelter almost complete

• Second 300 MW IPP unit in Balco capitalized

• Final terms for Vedanta Ltd and Cairn India merger announced, transaction to complete by this financial year

• Gross Debt for the Group reduced by c.US$ 0.3 billion during the quarter

Tom Albanese, Chief Executive Officer, Vedanta Resources plc, said: "We have made good progress on the ramp up of capacities at our Aluminium, Power and Iron Ore businesses during the quarter. These would be significant contributors to earnings as the year progresses…the simplification of the group structure, is also on track following the recent announcement of the revised and final terms for the Vedanta Ltd-Cairn India merger."

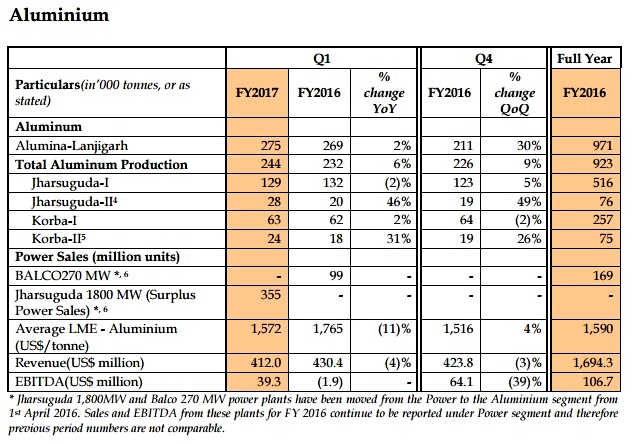

The ramp-up of pots at the Jharsuguda-II 1.25mt smelter started from 1st April 2016. The first line ramp-up is completed and the ramp-up at the second line has commenced in July 2016. Ramp-up commenced in mid-April 2016 at the 325kt Korba II smelter and 277 pots have been commissioned. Q1 reported a record production of 244 kt and the company achieved an exit run-rate of 1.1 mn tonnes in June 2016.

As a continuation of the approval for the expansion of the Lanjigarh refinery to 4 million tonnes per annum, the second stream of the refinery has re-started operations in this quarter. The company expects to produce 1.4mt in FY2017. Further ramp up to 4 million tonne is dependent on the availability of bauxite sources. In Q1, alumina production in Lanjigarh was 275,000 tonnes, which was a 30% rise QoQ.

From 1 April 2016, onwards the surplus power sales from the 1800MW from the Jharsuguda power plant, which has been converted to CPP for the Jharsuguda-II smelter is reported in the Aluminium segment. The 270 MW CPP at BALCO, has also been moved to the Aluminium segment from the same date.

Production cost of hot metal was $1,476 per tonne with Jharsuguda at US$1,459 per tonne and Korba at US$1,504 per tonne which was US$1,689 in Q1 FY 2016. The cost drop was primarily possible for the following reasons:

• Lower alumina and coal prices

• Rupees depreciation

• Implementation of various cost-saving initiatives

These were partially offset by addition of Clean Energy Cess and electricity duty. However, the cost has increased compared to US$1,431 per tonne in Q4 FY2016 due to urgent power purchases from the grid during a power outage and extra tax additions.

The EBITDA margin during the quarter maintained at $200 per tonne in line with the last quarter. The company targets 1.2 million tonnes of Aluminium production at a COP of c. $1,400 per tonne in FY2017.

Responses