您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

As the global economy pivots toward decarbonisation and circularity, recycled aluminium is stepping out of the shadows to become a material of strategic significance. The automotive industry is projected to register the highest usage of recycled aluminium during the forecast period, with manufacturers' marketing driven by the need for lightweight materials to improve fuel efficiency and reduce emissions.

Other sectors, such as packaging and construction, are integrating recycled aluminium into their net-zero targets as a key focus market; it is no longer just an environmentally sound option but an economic imperative.

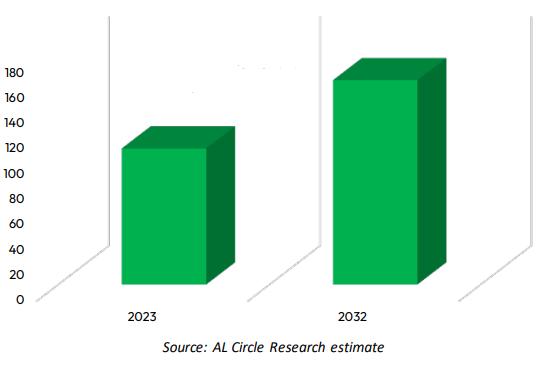

The world secondary aluminium market is projected to grow from USD 107.05 billion in 2023 to USD 160.81 billion by 2032, underscoring its critical role in shaping the future of low-carbon manufacturing.

Global aluminium recycling market size, 2023-2032 (in USD billion)

Unlike most industrial metals, aluminium can be recycled indefinitely without losing its core properties. The energy savings are staggering—secondary production consumes just 5 per cent of the energy required for primary aluminium. With ESG benchmarks becoming mainstream, industries such as automotive, packaging, and construction are increasingly turning to recycled aluminium to meet Scope 3 emission reduction targets and regulatory compliance.

According to China market analysis, the country leads the world in secondary aluminium production, with targets to peak carbon emissions by 2030 and achieve neutrality by 2060, propelling a shift from energy-intensive primary aluminium to low-emission secondary aluminium.

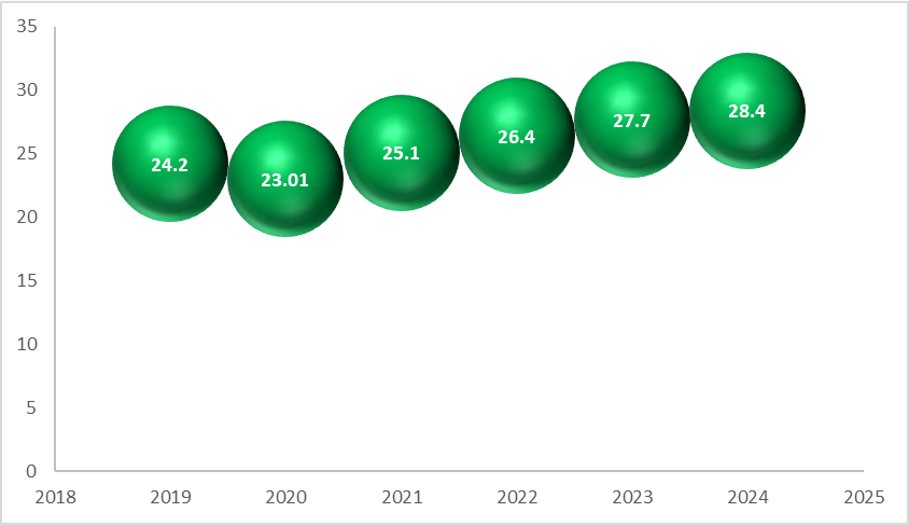

Global recycled aluminium usage, 2019-2024 (in million tonnes)

Source: AL Circle Research estimate

According to various business market research, Europe and North America are also expanding their remelting capacities and accelerating investments in scrap recovery and digital traceability tools to comply with tightening environmental mandates. Meanwhile, Southeast Asia and India are emerging as key processing hubs. However, challenges persist—chief among them being the shortage of high-quality scrap and the technological lag in some regions.

As a result, the policy of industry landscape analysis is also evolving. Instruments such as the EU’s Carbon Border Adjustment Mechanism (CBAM) are incentivising cleaner inputs, positioning recycled aluminium as a premium material in global trade. In light of the fact that more than 150 global OEMs have now included recycling clauses in their purchasing policies, a surge in demand for certified, low-carbon aluminium is on the rise, according to global market trends.

Aluminium scrap import trends (2020–2024)

As of May 2025, the global aluminium scrap import landscape reflects notable shifts in trade dynamics over the past five years. From 2020 to 2022, the world witnessed a steady increase in import volumes, rising from 9.53 million tonnes to a peak of 12.36 million in 2022—a nearly 30 per cent surge. This period marked a global industrial rebound post-pandemic and an accelerating transition towards circular economy principles. In 2023 and 2024, global imports slightly moderated to 11.94 million tonnes and 11.92 million tonnes, respectively. However, this marginal decline should not be interpreted as a fall in demand. Instead, it likely reflects tighter global scrap availability for trade, with many countries increasingly consuming more of their domestically generated scrap to meet rising internal demand for secondary aluminium.

However, in market statistics, a looming challenge persists: scrap scarcity. As demand outpaces collection, especially for post-consumer scrap, the industry faces rising input costs and capacity constraints. The global shift toward low-carbon or "green" aluminium is intensifying pressure on scrap availability. Regional markets are expanding remelting capacities and aiming to retain locally generated scrap to meet domestic demand.

The trajectory of the recycled aluminium sector is now more than simply speculation; it is now a matter of industrial urgency and strategic alignment. As global markets recalibrate in response to climate imperatives, policy pressures, and shifting supply chain dynamics, recycled aluminium stands at the confluence of environmental responsibility and economic opportunity.

However, the sector's future will not be defined solely by growth projections. It will be shaped by the industry's ability to secure high-quality scrap, modernise collection infrastructure, and deliver certified low-carbon material at scale. Without timely intervention, scrap shortages and regional disparities could undercut the very momentum that sustainability agendas seek to accelerate.

Responses