您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

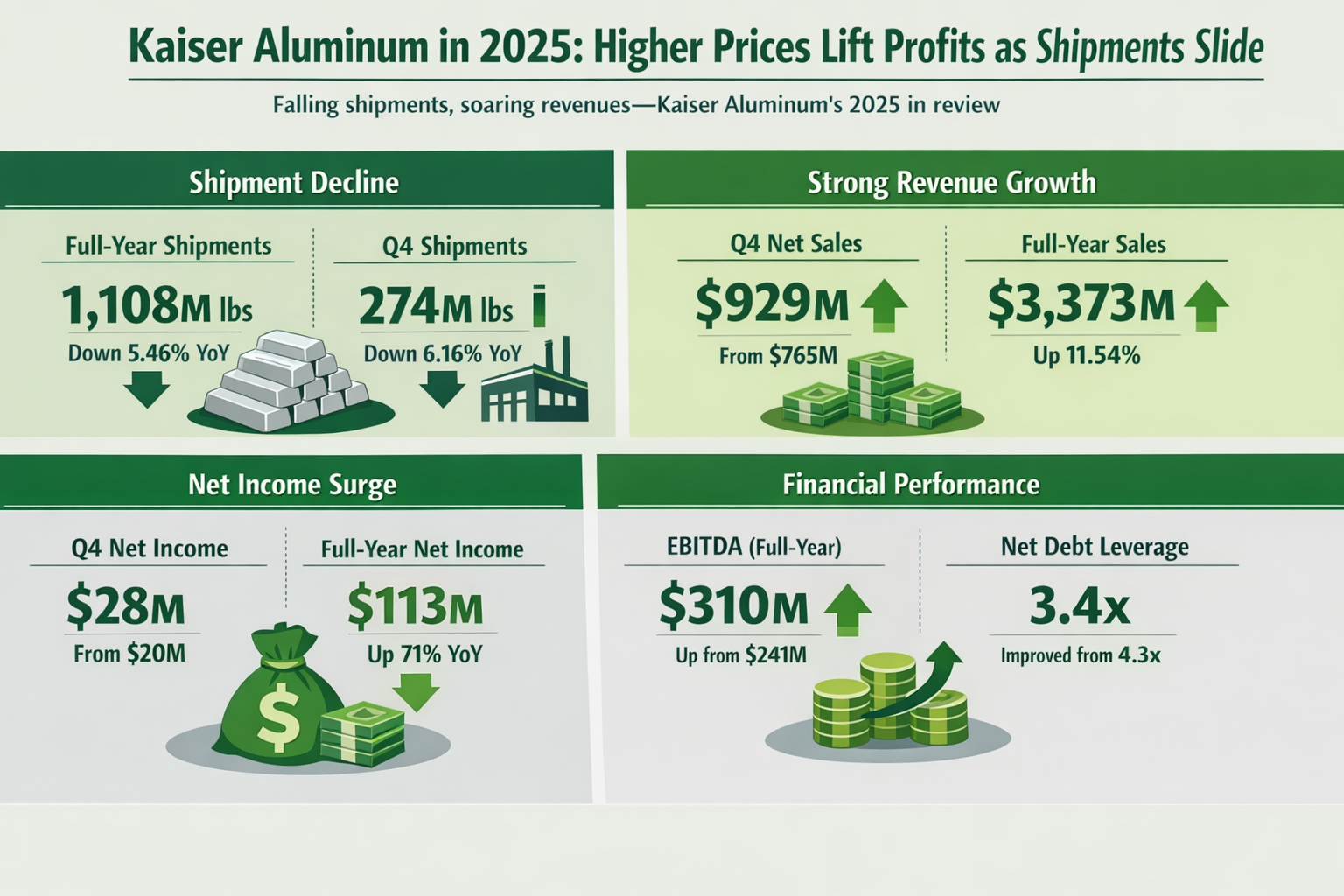

The delicate balance of falling shipments but rising revenues defined the aluminium industry in 2025, and so is the case for Kaiser Aluminum. The US-based producer of semi-fabricated specialty aluminium products closed the year with weaker shipments across most end markets yet delivered a sharply improved financial performance, riding on elevated aluminium prices and stronger pricing discipline.

{alcircleadd}Shipment volumes: A broad-based contraction

Kaiser Aluminum shipped 274 million pound (124,284 tonnes) of aluminium in Q4 2025, down by 6 per cent from 292 million pound (132,449 tonnes) in Q4 2024. Consequently, the company’s full-year shipments slipped 5 per cent Y-o-Y from 1,172 million pound (531,610 tonnes) to 1,108 million pound (502,580 tonnes).

Quarterly data underlined the persistent softness, with each quarter reporting Y-o-Y downfall. While in Q1, the shipments stood at 276 million pound (125,191 tonnes), down by 5 per cent Y-o-Y; in Q2 they amounted to 288 million pound (130,634 tonnes), although sequentially higher but 3 per cent less annually. Going into the third quarter, shipment volume dropped both Q-o-Q and Y-o-Y standing at 270 million pound (122,469 tonnes). However, in Q4, shipments gained 1 per cent sequentially, attributed to the ramp up of operations following the planned outage at its Trentwood facility in support of the Phase VII expansion and the benefit generated from improved coated packaging shipments at Warrick.

In product mix, only General Engineering saw a 5.6 per cent rise in quarterly shipments from 55.5 million pound to 58.6 million pound (26,580 tonnes). The full-year shipments of GE products also grew over the year from 228.7 million pound (103,736 tonnes) to 247.5 million pound (112,264 tonnes).

In contrast, aerospace sluminium shipments declined from 60.6 million pound (27,487 tonnes) in Q4 2024 to 46.8 million pound (21,228 tonnes) in Q4 2025. The full-year shipments totalled 204.8 million pound (92,895), significantly down by 16.5 per cent from 245.2 million pound (111,220 tonnes). Packaging aluminium shipments also contracted Y-o-Y in both Q4 and full-year, standing at 145.1 million pound (65,816 tonnes) and 560 million pound (254,011 tonnes) in the respective period. Similarly, automotive extrusion shipments declined and stood at 23.5 million pound (10,659 tonnes) in Q4 and 95.4 million pound (43,272 tonnes) in full-year.

Don't miss out- Buyers are looking for your products on our B2B platform

Revenue resilience: Pricing power at play

While volumes faltered, pricing dynamics worked decisively in Kaiser’s favour. At the end of December 2025, the global aluminium prices on London Metal Exchange reached USD 2,968 per tonne, potentially up by 13.6 per cent than the early September level. This strong aluminium prices translated into Kaiser’s positive net sales of USD 929 million in Q4, up from USD 765 million Y-o-Y.

In tandem with the rise in net sales, Kaiser Aluminum’s net income also grew over the year from USD 20 million to USD 28 million in Q4 2025. The US firm’s full-year net income stood at USD 113 million, recoding a 71 per cent hike Y-o-Y from USD 66 million. Net income per share, diluted, also increased in Q4 from USD 1.21 to USD 1.68, while that of full-year surged from USD 4.02 to USD 6.77.

Conversion revenue was USD 365 million in Q4 versus USD 358 million a year ago, while that in the full-year 2025 was USD 1,453 million compared to USD 1,456 million in 2024.

EBITDA also grew from USD 67 million to USD 88 million in Q4, reflecting an increase of 31.34 per cent Y-o-Y. It also grew sequentially by 8.6 per cent from USD 81 million. Kaiser’s full-year 2025 EBITDA was USD 310 million versus USD 241 million during the corresponding period of the previous year. The company’s earnings per share in Q4 were USD 1.53, which totalled USD 6.03 for the full year.

As of December 31, 2025, Kaiser’s net debt leverage ratio improved to 3.4x from 4.3x last year. The total liquidity it had was USD 547 million, consisting of cash and cash equivalents of USD 7 million and borrowing availability under the Company's Revolving Credit Facility of USD 540 million.

For 2026, Kaiser Aluminum expects conversion revenue to grow by 5 to 10 per cent and Adjusted EBITDA to climb up by 5 to 15 per cent.

Commenting on 2025 financial and operational results, Keith A. Harvey, Chairman, President and Chief Executive Officer, said: “Our fourth quarter performance reflected a year of consistent execution, marking our fifth consecutive quarter ahead of internal expectations and full year results that exceeded our 2025 outlook. Metal pricing remained a favorable tailwind, and despite non-recurring costs primarily associated with our new roll coat line and Phase VII planned outage, we delivered record full year adjusted EBITDA of $310 million with an adjusted EBITDA margin above 21%. We entered 2026 with a solid foundation, clear visibility into our end markets, and the capacity to capture the benefits from our recent major investments. We remain focused on cost reductions in manufacturing and operations and deleveraging our balance sheet while delivering meaningful value for our customers and shareholders in the year ahead.”

Responses