您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The energy industry attended ADIPEC 2025 with a familiar problem and left with a sharper one. Every major conversation in Abu Dhabi, whether on investment flows, upstream fuel security, grid volatility or the rapid buildout of digital energy systems, pointed to a structural shift already underway: the cost and carbon advantage of aluminium is no longer determined by the smelter, but by the energy system surrounding it.

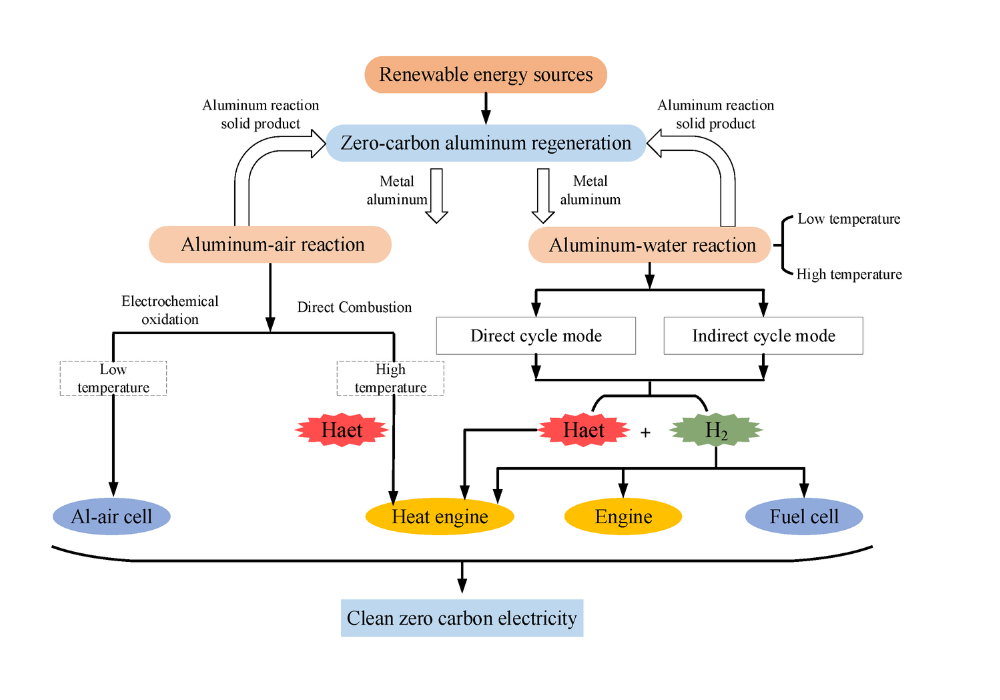

Image source: https://www.mdpi.com/

Image source: https://www.mdpi.com/

Explore- Most accurate data to drive business decisions with 50+ reports across the value chain

This is the unavoidable conclusion when the power consumption map from 2023–24 (Part 1 of this series) is layered against the messages coming out of ADIPEC. Smelters are now operating in an environment where energy is both their largest risk and their only meaningful decarbonisation lever.

And as the global energy transition collides with supply security concerns, the aluminium sector finds itself exposed on multiple fronts — from fossil-fuel price cycles to carbon border adjustments, from grid shortages to digital capacity gaps.

ADIPEC 2025 did not set out to answer aluminium’s questions. But the answers were there, in the subtext of every ministerial briefing and investment announcement: the energy equation that has insulated some aluminium regions and penalised others is about to get rewritten.

Energy supply tightening: Smelters will not be insulated from upstream shocks

…and so much more!

SIGN UP / LOGINResponses