您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

2018 first half has seen some unprecedented developments in the global alumina and aluminium market scenario that have turned the market upside down making all previous forecasts redundant.

The initiations

{alcircleadd}The aluminium supply scenario received the first hit when Trump imposed a global tariff of 25 per cent on steel imports and 10 per cent tariff on aluminium imported from all countries in March 2018. Though a few countries got exemptions on the tariff, all its major trading partners including Canada, Mexico, European Union and China were imposed heavy tariffs initiating the beginning of a long trade wars between these countries with the US.

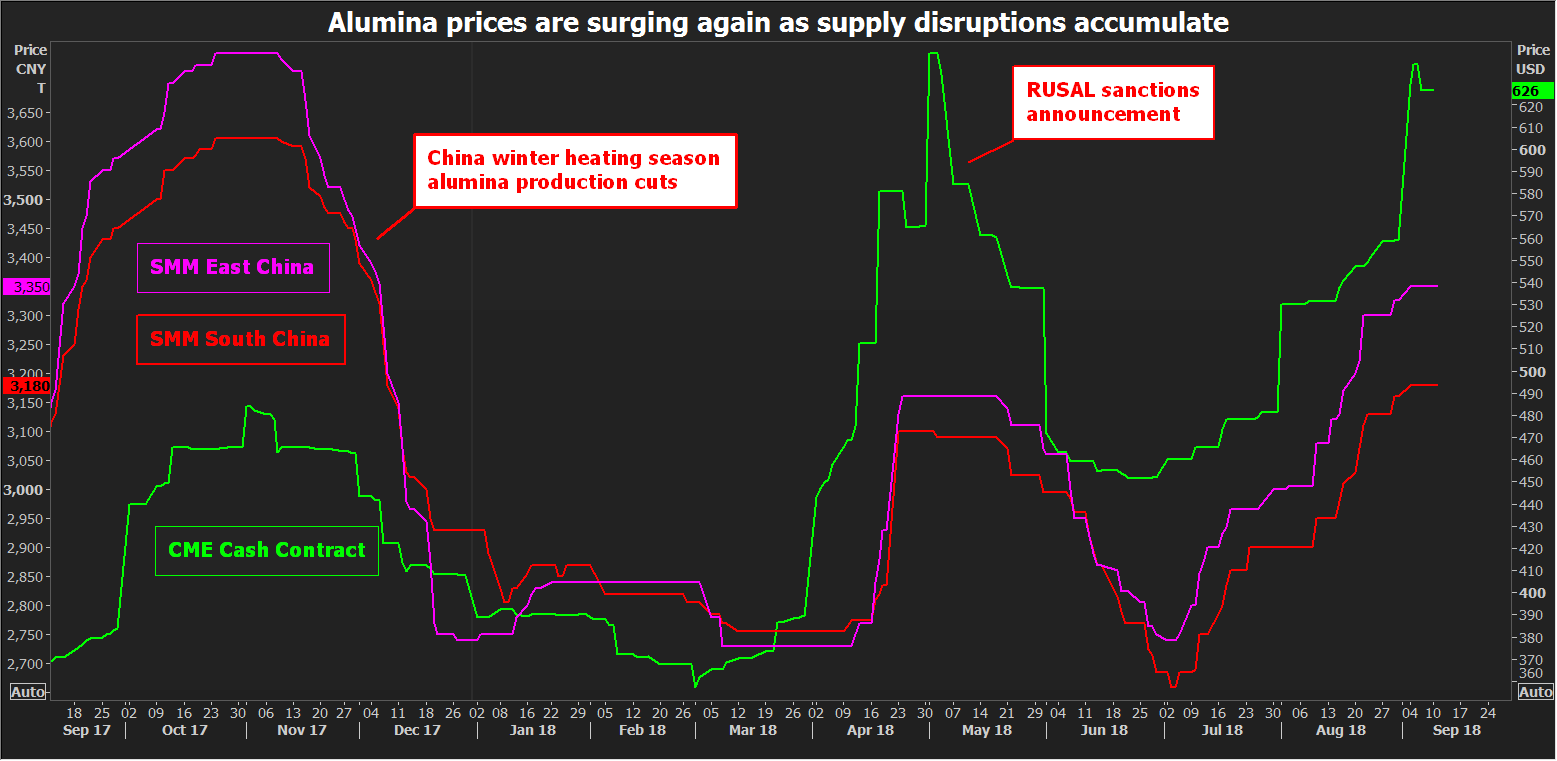

The supply scenario of alumina was disrupted by one major happening in the beginning of 2018. The fifty per cent capacity closure in Hydro’s Alunorte refinery in Brazil in March on the issue of bauxite residue pond leakage created panic in the market lifting the prices. However, prices were taken to an unforeseen level when, Trump administration imposed punitive sanctions on Rusal and its owner Oleg Deripaska on April 7 and following it, London Metal Exchange suspended Rusal’s aluminium from April 17.

Benchmark aluminium price on London Metal Exchange shot up to the highest in almost 7 years and closed at US$2602.5 per tonne on Thursday, April 19 from the previous day’s close at US$ 2528.50 per tonne. This was driven by panic buying as Rusal’s consumers as they feared they might not be able to buy or trade metal from Rusal. The prices started correcting during the end of April when the Treasury had extended its deadline for U.S. consumers to wind down business with Rusal to Oct. 23, but still the prices continued to stay bullish.

Rusal accounts for about 14 per cent of world aluminium production outside China. The company not only supplies about 6.5 % of global aluminium demand but also supplies about 7 per cent of the world’s alumina, with plants in Ireland, Jamaica and a 20 per cent stake in Rio Tinto’s giant refinery in Queensland, Australia. Spot alumina price saw some unprecedented highs in 2018 first half and doubled to over $700 per tonne as the market showed panic reaction to U.S. sanctions on Rusal in April.

Australia Alumina FOB Price (US$/t)

The sanctions put the future of Rusal’s Aughinish alumina plant in doubt, which is Europe's largest alumina refinery in Ireland and a major alumina asset of RUSAL contributing about 30 per cent of alumina produced in the EU. Though Aughinish won a reprieve after the extension of deadline, alumina prices have not gone back to the pre-sanction level on uncertainties surrounding supply. Australia Alumina FOB price and China’s domestic spot alumina prices have corrected to a certain extent in June but the prices started recovering again on supply uncertainties and more disruptions coming up in the Australian alumina sector.

Present Scenario (Alcoa refinery strike, Hydro Alunorte, China winter capacity cut)

Image: Reuters

Image: Reuters

Around 1,500 of its 1,600 workers at Alcoa’s Wagerup, Pinjarra and Kwinana refineries and the Huntley and Willowdale bauxite mines walked out of work on August 8 over a new workplace agreement. The walk-out at the refineries has injected yet more uncertainty into an already problematic supply equation. A likely resolution of workers’ strike at AWAC’s refineries can improve the supply situation in alumina.

Rusal’s parent company has been negotiating with the US Treasury to free itself from the sanctions; however, it is not clear if the sanctions will be lifted. The US Treasury has extended a deadline for the full imposition of sanctions against the aluminium empire of Oleg Deripaska, giving the company another three weeks to find a way to win a full reprieve. Late on Friday, September 21, the Treasury said it would extend the deadline to November 12. The owners of the Aughinish Alumina refinery in West Limerick have secured a temporary reprieve over threat to alumina jobs from the Trump administration after the news of the three-week extension had arrived.

Norsk signed two agreements on September 5 towards restarting of operations in Alunorte. But in order to resume full output at the 6.3m tonne a year alumina refinery, Hydro needs a Brazilian court to lift the five production embargoes. Norsk Hydro is striving to convince Brazilian authorities to allow it to resume full production at Alunorte refinery. The deals, signed on September 5 in Brazil, were an important step but did not guarantee to allow full resumption of production at Alunorte, John Thuestad, Norsk Hydro’s executive vice-president for bauxite and alumina, told Reuters.

Graham Kerr, mining group South32’s chief executive, said market disruption showed no signs of easing as the market would face another supply scarcity when China will start the second year of environmental capacity cut in the country in winter season. The Ministry of Industry and Information Technology said on its website in the first week of August that China would continue output cuts in the domestic alumina/aluminium sector during the coming winter heating season (November 15-March 15) and the aluminium and alumina sectors will both be required to cut 30% or more of its capacity.

A medium term forecast

The extension of Sanctions against UC Rusal by the US Treasury indicated softening of US Sanctions against UC Rusal. The Treasury allowed UC Rusal's current and past clients to transact with them in the spot and contract market past October 23, based on their business relations prior to the impositions of the Sanctions. However, no company can agree new contracts beyond that date unless sanctions are lifted. Friday’s announcement is big news to the market as it is considered as a hint towards lifting of sanctions against UC Rusal. Only then, Rusal would supply alumina to primary aluminium smelters in Europe from its alumina refineries.

We continue to see a bullish market for alumina in the last quarter of 2018 till the first quarter of 2019. Though there are indications that the situations will improve, the Alcoa refinery Strike, and the bureaucratic negotiations that Norsk Hydro is undergoing do not seem to be resolved any sooner. This will further be pressurised if China resumes winter capacity cuts.

Graham Kerr, mining group South32’s chief executive said it would still be “difficult” for the Alunorte refinery to return to full production this year. Commenting on China’s seriousness about winter capacity cut, he said that “The blue-sky policy is real.”

According to the latest update by Shanghai Metals Market, alumina production in Lvliang of Shanxi province is likely to be affected as the area was highlighted in China’s three-year initiative to “make skies blue again”. Restarting of operations is also much slower than expected.

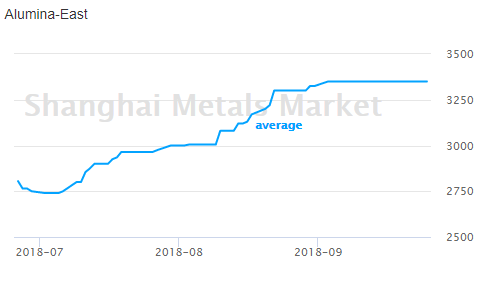

East China Average Alumina Price (RMB/t)

Domestic alumina spot prices in China are cheaper than alumina from Australia, which is driving Chinese companies to export alumina. Though China exports very less of alumina, the country’s alumina export has seen a solid growth since April. Australian FOB price stood at $626 per tonne in the second week of September, just shy of the record $643 seen at the start of May and has recently come down to US$ 535 per tonne after the extension of Rusal sanction. According to Shanghai Metals Market, China average spot alumina prices dropped to RMB 3284 (US$478) per tonne now, from RMB 3302 (US$ 482) per tonne in September begining, the highest since December 2017. In East China market, the prices now stand at RMB 3350 (US$488) per tonne, still much higher. The lowest level the alumina prices have touched in 2018 was about US$ 370 per tonne and the level is not expected unless all current supply disruptions come into place.

UAE’s Emirates Global Aluminium (EGA) has received the first shipment of caustic soda for its under-construction Al Taweelah alumina refinery in September. The company also began importing bauxite in June 2018 from the Republic of Guinea and stockpiling hydrate, another raw material for the refinery. Once full ramp-up is achieved, the refinery is set to produce about two million tonnes of alumina per year. The first alumina from Al Taweelah alumina refinery is expected during the first half of 2019. We expect alumina spot prices to average $400 per tonne only in H2 2019, when winter production cuts in China will be over and EGA would be ramping up production of their refinery.

During Q2 2018 results, Alcoa projected a full-year 2018 global deficit for both aluminium and alumina. For alumina, the company projected a slightly lower global deficit between 200 thousand and 1 million metric tons. Alumina prices will continue to be under pressure and the market will remain tight in partial absence of two major producers in operations and another one struggling with workers strike, while China is going ahead with alumina capacity cut in winter.

Responses

_0_0.jpg/500/0)