您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The global transition toward low-carbon or "green" aluminium is no longer a distant ambition—it's reshaping the very foundation of the secondary aluminium market. Driven by sustainability commitments, rising consumer expectations, and stricter regulations, the pressure on scrap availability is intensifying. This imbalance between capacity expansion and supply growth has set the stage for fierce competition that spans continents.

Source: Recycling Today

Scrap at the heart of the green transition

From 2019 to 2024, secondary aluminium capacity witnessed steady growth. But the real surge is just ahead: between 2024 and 2026, planned capacity expansions will significantly outpace scrap availability. This widening gap raises a critical question: Will the industry secure enough feedstock to fuel its low-carbon future?

Used beverage cans (UBCs) and extrusion scrap are emerging as the tightest supply bottlenecks. Demand growth is outstripping collection rates, while sorting and recycling technologies, though improving, are still insufficient to close the gap. Regional markets are increasingly focused on retaining domestically generated scrap, with Europe and North America facing competition from Asia—particularly China—for material access.

Looking for actionable insights into one of the fastest-growing segments in the global metals industry? The updated "World Recycled Aluminium Market Analysis – Industry Forecast to 2032" delivers exclusive data on market trends, regional demand, trade, policy shifts, technology, and competition.

China: The centre of gravity in recycled aluminium

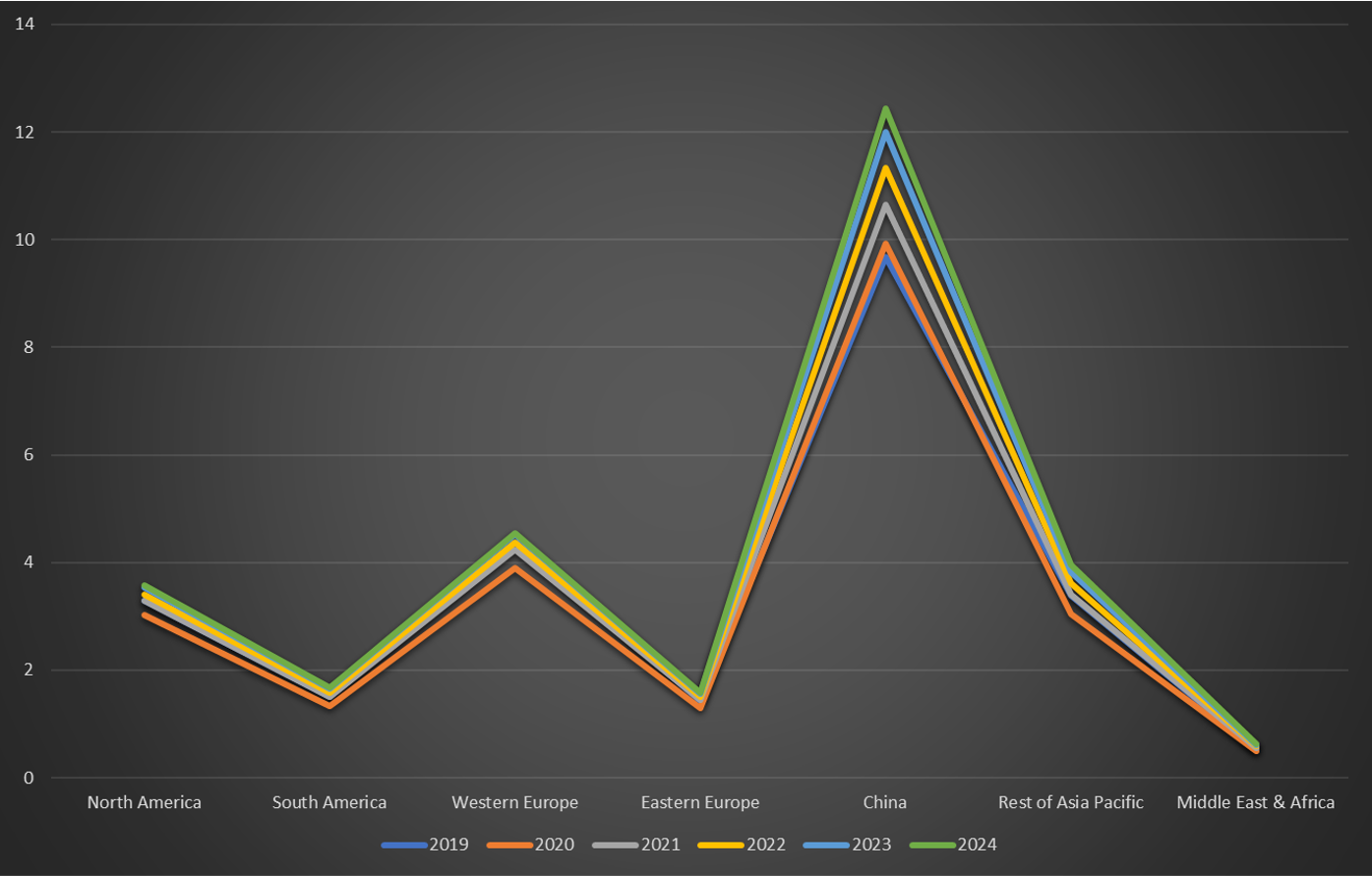

A closer look at the China market analysis underscores the country's dominance in shaping global dynamics. In 2023, China consumed 12.01 million tonnes of recycled aluminium, and forecasts suggest usage will surpass 14 million tonnes by 2026, with even stronger growth by 2030, as per AL Circle's Research. Regulatory reforms have added another layer of complexity: restrictions on aluminium scrap imports and stringent quality standards have tightened inflows, making domestic scrap retention and secondary production more critical than ever.

World recycled aluminium usage by region & country 2019-2024 (in million tonnes)

Source: AL Circle Research; Industry Publications

World Recycled ALuminium Market Analysis Industry forecast to 2032

For Europe, which has historically exported significant scrap volumes, this trend is transformative. European market research perspective shows that the continent now faces the dual challenge of competing with Asia for material while ensuring adequate local supply for its own growing remelting capacity.

Market shifts: Billet and slab leading the charge

Capacity additions tell their own story. Between 2022 and 2026, billet production will account for nearly 50 per cent of new secondary aluminium capacity—equivalent to 11 million tonnes. Slabs follow with 40 per cent (8.8 million tonnes), driven by robust downstream demand in automotive and packaging. Interestingly, 2025 marks a sharp spike in new capacity (6.4 million tonnes), likely reflecting slab-focused investment aligned with rising demand for canstock and automotive sheet.

By contrast, secondary foundry alloys (SFA) represent only 10 per cent (2.2 million tonnes) of new capacity, indicating that the ingot market is comparatively saturated. This realignment is a clear reflection of industry trend analysis, where demand pull from packaging and mobility is reshaping product priorities.

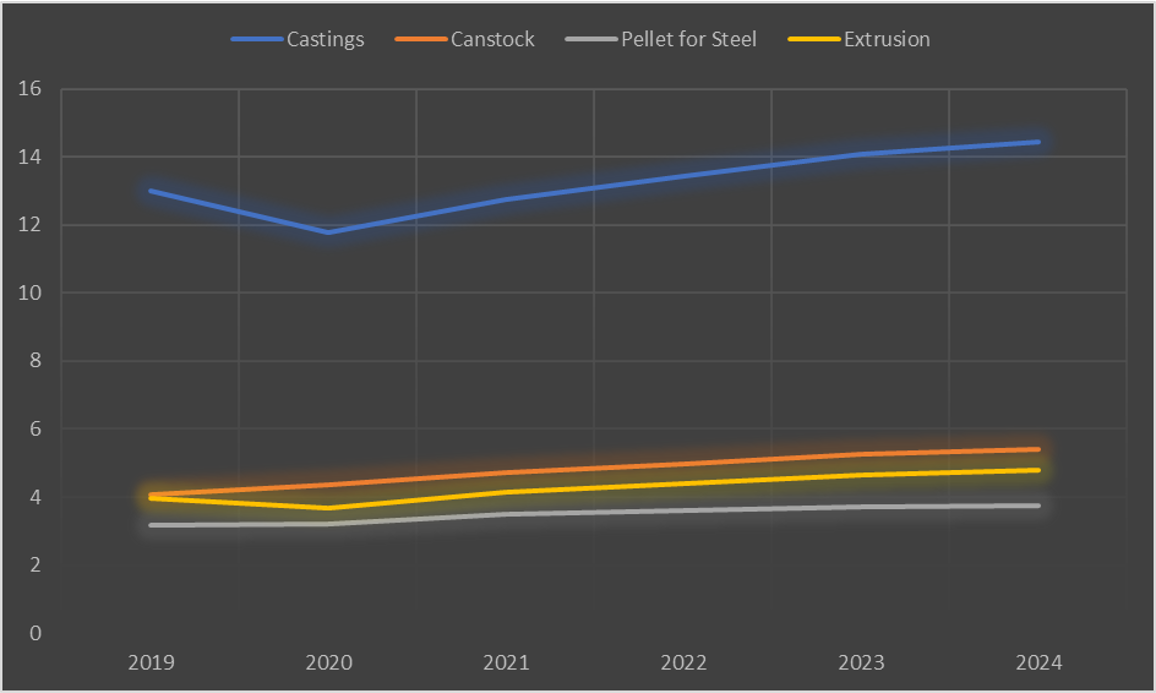

Sectoral demand dynamics

A deeper market size analysis of end-use applications reveals telling trends:

Canstock: In 2020, Canstock was the only recycled aluminium application to record growth, highlighting its resilience even during economic shocks. By 2023, demand reached 5.25 million tonnes, and climbed further to 5.42 million tonnes in 2024, cementing its role in packaging sustainability.

Looking for insights into the fast-evolving aluminium flat rolled products market? "Aluminium Flat Rolled Products: Insights & Forecast to 2030" covers global trends, grade-wise demand (1XXX, 3XXX, 5XXX), and key end-use sectors. From regional shifts to industrial drivers, it’s your roadmap to understanding this vital industry.

Castings: After pandemic-driven declines, global casting demand rebounded to 14.09 million tonnes in 2023 and further to 14.44 million tonnes in 2024, supported by the automotive sector's recovery.

Extrusion: Demand increased steadily to 4.80 million tonnes in 2024, signalling strong momentum in construction and industrial sectors.

Pellets for Steel: Remaining relatively stable, this segment posted 3.72 million tonnes in 2023 and 3.74 million tonnes in 2024.

Global recycled aluminium usage by end use, 2019-2024 (in million tonnes)

Source: AL Circle Research; Industry Publications

World Recycled ALuminium Market Analysis Industry forecast to 2032

This industry trend research confirms that automotive remains the strongest pull factor, particularly for secondary aluminium alloys such as ADC12 and A380.

The road ahead: Competition, consumers, and capacity

The global recycled aluminium market is at a crossroads. Capacity growth is outpacing scrap collection, and China's structural reforms continue to redirect global flows. Europe and North America, once comfortable exporters, are increasingly compelled to safeguard their scrap resources. Meanwhile, consumer demand for low-carbon products—from beverage cans to EVs—will only intensify.

For stakeholders, navigating this landscape requires not just operational agility but also access to reliable intelligence. According to a consumer research report, the approach—combining insights from material flows, capacity expansions, and sectoral demand—is becoming essential for investors, manufacturers, and policymakers.

The race for green aluminium is, in essence, a race for scrap. As we move closer to 2030, the winners will be those who can secure supply, adapt capacity, and align with the fast-evolving expectations of global consumers.

Responses