您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

2021 was a year of recovery for the global aluminium industry from unpleasant impacts of the COVID-19 pandemic. Right from the demand and usage to production, the aluminium industry underwent a revamp across all its value chain throughout the year 2021. Though the aggregate demand rose impressively through the year, many end-use sectors were yet to witness a full recovery from the 2020 set-back. While the packaging industry performed extremely well driven by beverage cans and pharma packaging, automobile production was far from reaching the pre-covid levels.

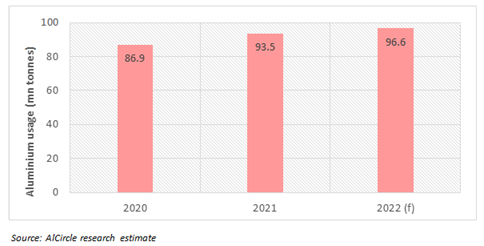

The worldwide aluminium usage increased from 86.9 million tonnes in 2020 to 93.5 million tonnes in 2021, underpinned by 7.6% of demand growth in the same year. Production also expanded by 2.6% to 67 million tonnes but remained much behind the consumption volume, causing a demand-supply gap. In the current year, the demand is estimated to grow further to stand at 96.6 million tonnes.

{alcircleadd}Figure 1: World aluminium demand, 2020 to 2022 (million tonnes)

As the industry was resonating in the previous year, a positive effort in making a sustainable market was also seen, and therefore, changes in policies influenced by climate agreements reached the international level. It is to be mentioned here that the use of recycled aluminium increased by about 7% to stand at 26 million tonnes in 2021.

It is needless to say that after this stimulating year in the aluminium industry, the market leaders and shareholders are eagerly looking forward to 2022 and busy in projecting how the year will shape up the entire value chain of the industry.

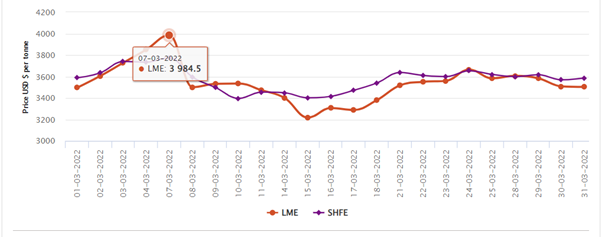

In the China market, the aluminium price is estimated to increase in 2022 on the back of increasing demand from end-use sectors and with the country’s capacity cap of 45 million tonnes of primary aluminium per year. So far this year, what has primarily driven the price growth is the Ukraine-Russia war, which has caused disruptions in the worldwide supply chains of raw materials, resulting in primary metal production hindrance. In early March, the A00 aluminium ingot price in China reached as high as RMB 23,860 per tonne, while the LME price during the same time grew 13-year high at US$3,984.50 per tonne.

Figure 2: LME aluminium price at 13-year high in 2022

Coming to the upstream production, primary aluminium output across the world slumped in February by 9.34% month-on-month to 5.114 million tonnes, according to the International Aluminium Institute (IAI). So was the output of alumina as well, which decreased by 8% on the month to 10.606 million tonnes.

In late February, Russian aluminium producer Rusal halted alumina shipments from its 1.75 Mtpa Nikolaev refinery in Ukraine. That narrowed the supply chain with only weeks of alumina stocks on site rather than months, impacting the primary aluminium production. Wood Mackenzie analyst Ami Shivkar noted that Nikolaev’s alumina is transported to the Bratsk, Krasnoyarsk and Sayanogorsk smelters in Russia which together produce 2.5 million tonnes a year.

The Australian Department of Industry had projected that the global alumina price would hover around $345 per tonne, an increase from the revised price of US$325 per tonne in 2021.

However, many leading companies of the industry such as EGA think this unusual price surge of the primary metal is a short-term issue. So, the company has pledged to keep expanding their productions to meet the rising demand. According to a recent study published by CRU International on behalf of the International Aluminium Institute (IAI), global aluminium demand will rise by almost 40% to 119.5 million tonnes at the end of 2030, which will require an additional 33.3 million tonnes of production. Hence, is mulling to expand the midstream and downstream aluminium industry, such as auto-spare parts, according to Mr bin Fahad.

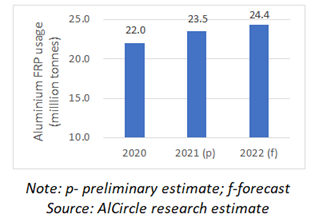

It has been already estimated that aluminium usage in the automotive market will grow strongly in the second half of 2022 after a subdued growth in H1. Worldwide aluminium FRP (excl. foilstock) usage is projected to grow at about 3.8% to reach 24.4 million tonnes by 2022. The aluminium autobody sheet, which had been growing impressively before the pandemic, is expected to resume growth from 2022 onwards.

Figure 3: Global aluminium FRP usage trend and forecast, 2020 to 2022 (million tonnes)

The demand for recycled aluminium is also expected to grow at a healthy pace of about 4 to 5% per annum during the next few years, primarily contributed by Asia Pacific region outpacing the rest of the world.

Overall, the year 2022 is estimated to witness a continued growth in demand but at the same time projected to face challenges like energy crisis, supply chain disruption, and escalating prices of raw materials. Amid all this, it is important to know the opinions of industry leaders and enthusiasts, and hence, the AlCircle team has brought to you its famous line of e-Magazine yet again “LeaderSpeak 2022”. Let us here discover the beliefs and viewpoints of some of the most eminent companies in the industry so to be able to take the right decision on investments and expansions for the year and beyond.

Responses