A recent market analysis indicates that the global food tins and drink cans market including aluminium is poised for steady growth, with its value expected to rise from an estimated USD 2.6 billion in 2025 to a solid USD 4.0 billion by 2035. This expansion, fuelled by a compound annual growth rate (CAGR) of 4.5 per cent, reflects the increasing consumer demand for convenient, durable, and eco-friendly packaging solutions. The report underscores how the market is evolving in response to the global push for sustainability and the growing popularity of ready-to-eat meals and beverages.

A major driver is the growing demand for extended shelf life and efficient storage solutions. Metal packaging, especially aluminium and steel, plays a vital role in preserving product quality by safeguarding contents from contamination and oxidation. This is essential for a variety of products, including dairy, ready-to-eat meals, fruits, vegetables, and pet food. Additionally, the increasing emphasis on convenience, alongside the rise of urban living and dual-income households, has heightened the demand for packaging that fits seamlessly into modern lifestyles.

Outlook for aluminium packaging sector

In 2023, the aluminium packaging industry saw consistent growth, fuelled by rising demand for beverage cans and packaging foils. With over 11.5 million tonnes of aluminium flat-rolled products used in packaging, the shift from traditional materials like plastic and glass to aluminium has paved the way for a dynamic evolution in the sector.

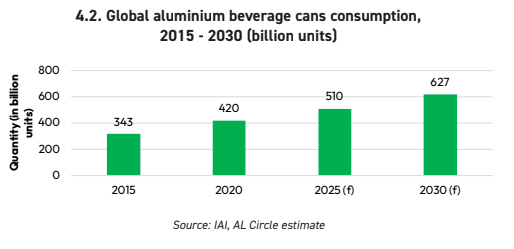

As per AL Circle’s report, the Global consumption of aluminium beverage cans rose from 343 billion units in 2015 to 416 billion in 2020, with projections estimating that by 2030, global production will soar to 627 billion units.

Get more insights on the packaging sector - ALuminium in Packaging: Consumer Trends and Market Dynamics

In 2023, the global aluminium cans market was valued at USD 55.5 billion, with expectations to reach around USD 85.6 billion by 2032, expanding at a compound annual growth rate (CAGR) of 4.93 per cent. The growing consumption of beverages is anticipated to be a major driver of the aluminium cans market in the coming years, with aluminium cans available in various sizes, further boosting demand.

In addition to beverages, aluminium cans are seeing increased use in food packaging, and their popularity is expected to rise significantly. The introduction of BPA-free aluminium cans, offering chemical-free packaging, is set to spur further growth, particularly in developed nations where demand for canned foods is growing. As more consumers seek safe, sustainable options, the aluminium can market is poised for a bright future.

Region wise demand for aluminium cans

North America remains the leading consumer of aluminium beverage cans globally. The North American market for aluminium beverage cans is projected to grow from 120 billion cans in 2020 to 173 billion by 2030, reflecting a CAGR of 3.73 per cent. By 2030, North America is expected to represent 25 per cent of the global aluminium can market.

Demand for aluminium beverage cans in Europe has grown significantly, driven by key sectors such as soft drinks, water, beer, and seltzers. Over the next decade, the EU is set to undergo a complete transition from tinplate to aluminium cans, with Ball Corp and Crown leading the shift in France and Spain. Production of aluminium cans in Europe is forecast to rise from 73 billion units in 2020 to 109 billion units by 2030, growing at a CAGR of 4.09 per cent.

The adoption of aluminium cans is rapidly growing in developing markets like India, with several global can manufacturers setting up production facilities in the country. Key sectors driving this demand include soft drinks and beer, while emerging segments like sparkling water, wine, and hard spirits are expected to further boost consumption. In 2019-20, India consumed approximately 1.3 billion aluminium beverage cans, and this figure is projected to reach 2.5 billion units by 2029-30, growing at a CAGR of 6.76 per cent. India's recycling rate for used aluminium cans stands at around 85 per cent.

Aluminium production in China is expected to grow from 71 billion units in 2020 to 122 billion units by 2030, with a CAGR of 5.56 per cent. This growth is primarily driven by the shift from glass bottles to canned beers, along with a moderate rise in soft drink consumption. Currently, over 70 per cent of aluminium beverage cans are recycled into new products; however, this recycling rate still falls short of the levels needed to meet the 1.5-degree climate target.

Demand for aluminium beverage cans is rising in South America, with Canpack Group investing in a new facility in Minas Gerais, Brazil, to manufacture cans. This plant is set to have an annual production capacity of 1.3 billion cans and is expected to begin operations by 2024. Brazil ranks as the third-largest market globally for aluminium beverage cans, with sales reaching 33.4 billion units in 2021, a 5.2 per cent increase from the previous year. According to the Brazilian Aluminium Manufacturers Association, the country boasts the highest recycling rate of used aluminium cans worldwide, at an impressive 98.7 per cent.

The demand for aluminium in packaging is primarily driven by the beverage can market. While developed economies have long embraced aluminium cans, emerging markets are now catching up at an even faster pace. However, one challenge could be the potential risk of downgauging, which could dampen growth prospects. The rise of younger consumers, new product varieties, and increasing environmental awareness has boosted the demand for beverage cans. Looking ahead, the aluminium packaging industry is expected to keep soaring over the next five to seven years. The surge in demand is driven by a growing preference for eco-friendly packaging, higher disposable incomes, and urbanisation. But it’s not just about demand cutting-edge technology is also transforming the market.

Also Read: Pakistan-based aluminium can manufacturer increases production volume

Responses