您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

![]()

In this exclusive conversation with AL Circle, Mario Conserva highlights the growing strategic importance of aluminium scrap in Europe’s transition toward a low-emission and circular economy. He emphasises how rising scrap exports are weakening domestic industry competitiveness and calls for urgent action to secure secondary raw materials within Europe, stabilise prices, and ensure the region’s industrial resilience amid high energy costs and evolving geopolitical pressures.

Mario Conserva, Secretary General of FACE and a veteran with over six decades in the aluminium industry, brings unmatched expertise as founder of METEF, leader of A&L Alluminio e Leghe, and a pioneering contributor with 800+ technical works. Recognised by the IAI as one of the 50 most influential global aluminium figures, he continues to shape policy, innovation and downstream competitiveness across Europe.

Note: While you continue reading, refer to the graphs at the hyperlinked "Figures" to access the data and gain insights on the EU scrap export scenario.

AL Circle: You have emphasised that scrap is vital for a competitive, low-emission aluminium sector. Would you quantify the economic and environmental value of retaining scrap within Europe?

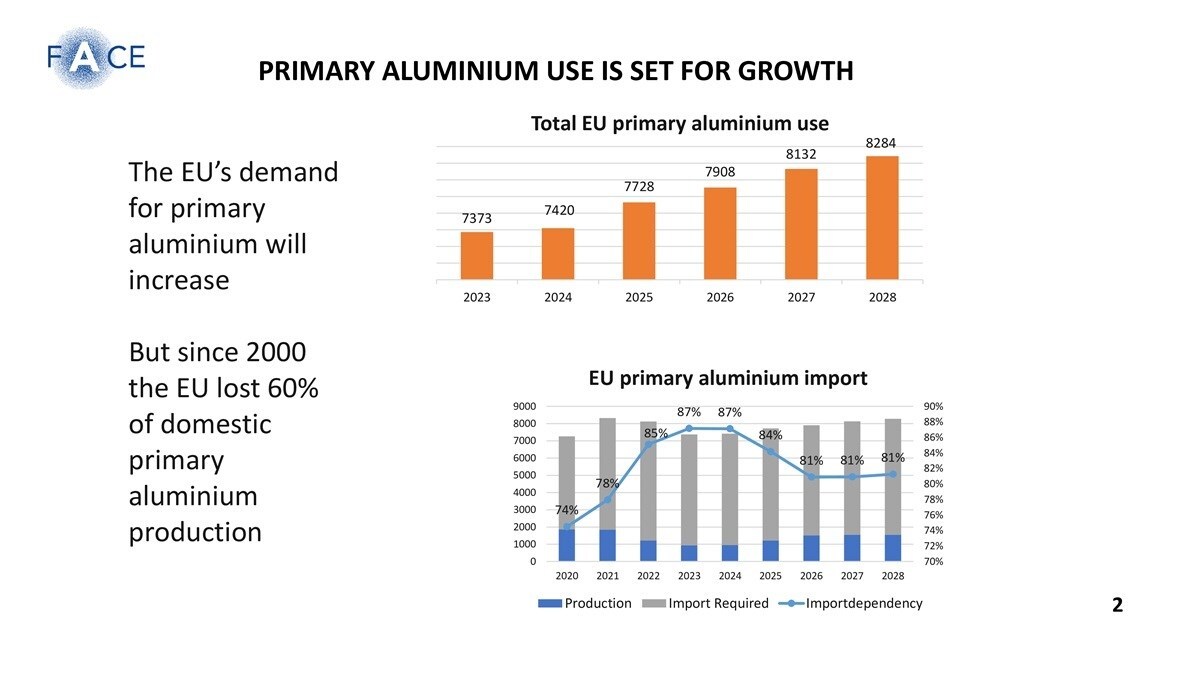

Mario Conserva: Today and in the near future, with primary aluminium production gradually declining, and final uses set for growth (Figure 1; Figure 2), the EU is more and more dependent on secondary material (Figure 3).

FACE representing since more than 25 years independent downstream transformers consumers and end users of aluminium in Europe, strongly defends the aluminium value chain (Figure 4; Figure 5; Figure 6), today characterised by structural primary metal deficit exceeding 87 per cent of the use (Figure 7), with a demand currently standing at more than 8 million tonnes per year, that according to some estimates, could double by 2050.

AL Circle: Europe exports more than 1.2 million tonnes of aluminium scrap, much of it to Asia. In your experience, to what extent is this “scrap leakage” adversely affecting the competitiveness and investment prospects of EU recycling SMEs? Given the massive amount of scrap being exported due to insufficient raw material demand and possibly underutilised recycling capacity within Europe, what investments or incentive mechanisms does FACE believe would unlock such capacity in Europe?

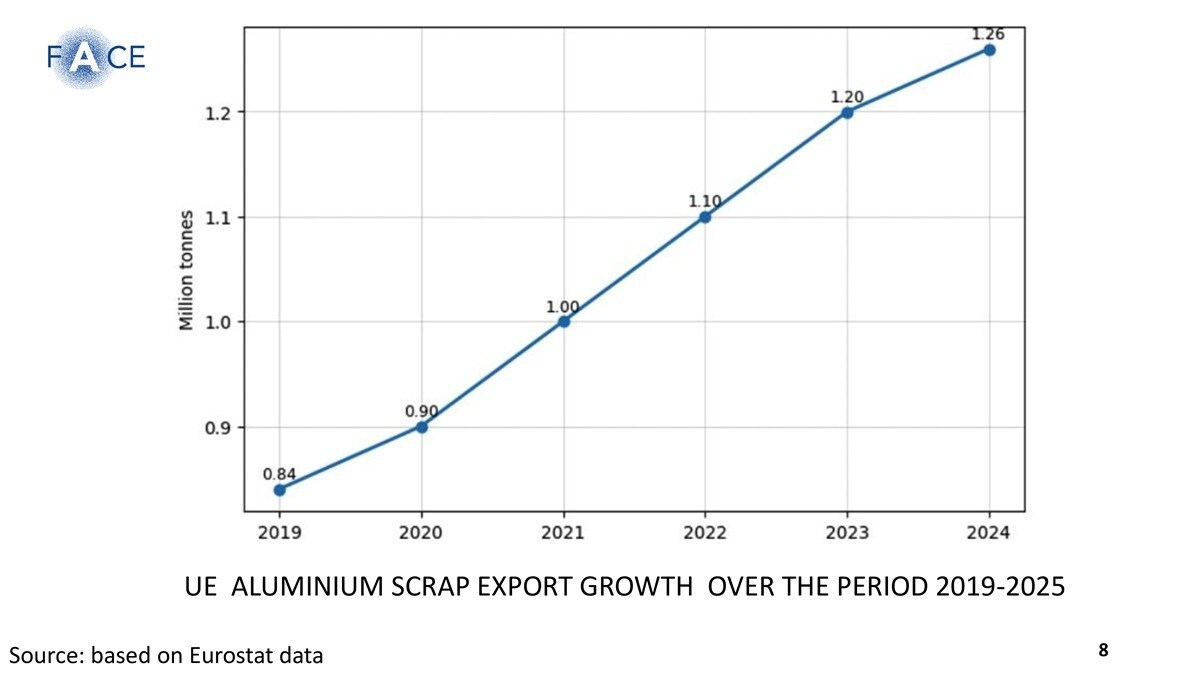

Mario Conserva: The current leakage of aluminium scrap (Figure 8), whereby we gift 1.2 million tonnes of this strategic resource to third countries annually, has reached a breaking point. This volume represents nearly 25 per cent of Europe’s total recycling capacity, and we should improve it inside.

We cannot claim to seek "strategic autonomy" while allowing our most energy-efficient feedstock to be drained. The centre of our proposal is the introduction of a significant export tariff on aluminium scrap. The objective is to curb price arbitrage towards third countries, where operators may benefit from state subsidies, lower environmental standards or non-equivalent competitive conditions. These dynamics, our and other associations and companies warn, are draining valuable secondary raw materials from the EU market at a time when securing domestic supply is increasingly strategic.

AL Circle: Do you see a direct link between scrap exports and the decline in Europe’s primary aluminium capacity, which is below 15 per cent of demand? How urgent is the need to address this imbalance?

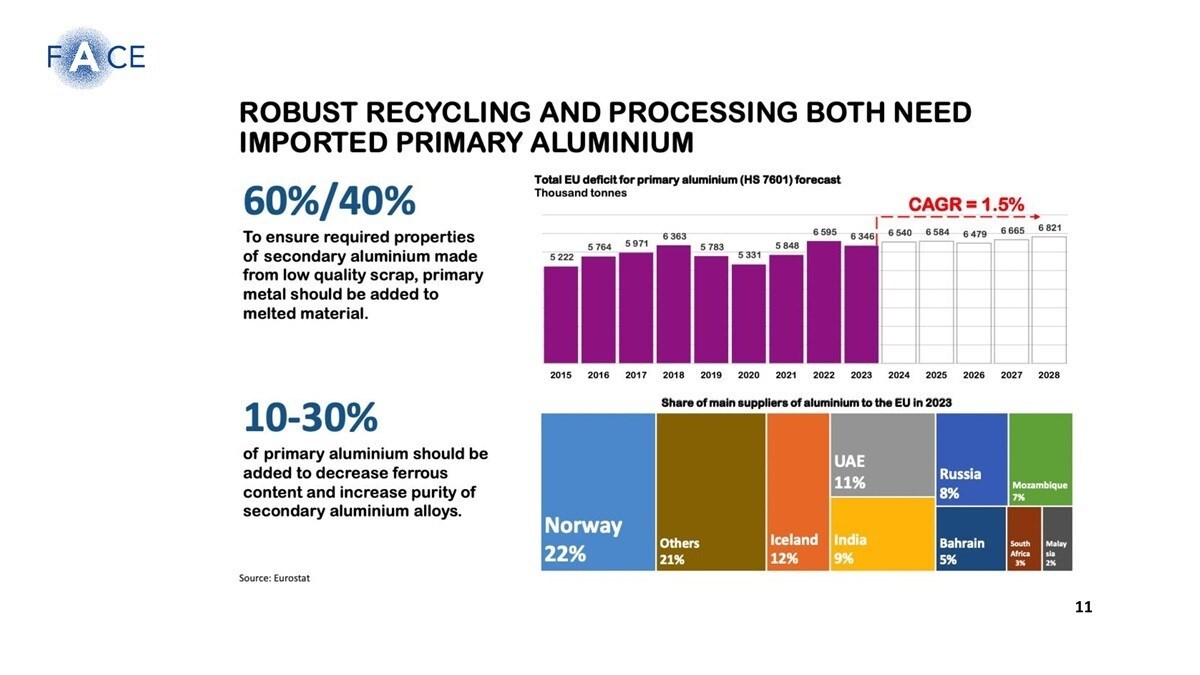

Mario Conserva: I see no connection between the decreasing production capacity of primary unwrought aluminium, largely driven by the rising energy costs of electrolytic metal production (Figure 9), and the growing export of aluminium scrap. The fact is that we must purchase in more than 7 million tonnes of primary metal annually, ed in parallel we are doing an excellent work in scrap recovery and recycling of the precious secondary metal, a significant global action (Figure 10) which requires only 5 per cent of the energy needed for primary production; the problem is that the EU aluminium scraps are largely exported to third countries (Figure 11) that are also in strong competition with Europe on the global aluminium market scraps, including industrial waste and end-of-life products, are by sure increasingly important in the aluminium industry, as being the most energy efficient method of producing the metal: remelting aluminium for new uses requires in fact from 90 to 95 percent less energy than primary electrolytic metal. Not surprisingly, secondary production is increasingly regarded as highly suitable for the European Union, also because of the increasing quantities of domestically generated scrap available within the region.

AL Circle: You have advised on recognising aluminium scrap as a strategic secondary raw material, and FACE has called for “targeted measures” to retain scrap in Europe. Which approaches would you advocate, such as implementation of export tariffs, licensing systems, or quality/traceability requirements, for that to be most effective?

Mario Conserva: The underlying drivers are well known: strong global demand for scrap, combined with distortive subsidies and lower regulatory constraints in certain third countries, allows non-EU operators to consistently outbid EU recyclers. The result is a sustained outflow of EU-generated scrap at a time when European demand for secondary aluminium is rising. After having heard what other stakeholders and we had to say on the matter, the EU Commission launched a consultation on which measures to take to ensure the availability of aluminium scrap on the EU market. We welcome the Commission’s call for evidence on a necessary trade measure, stressing that the downstream segment of the aluminium chain in the EU constitutes 70 per cent of the industry’s turnover and 90 per cent of its workforce. For our companies, access to affordable secondary aluminium is a decisive factor for competitiveness and investment, and, as the EU Commission points out, scrap prices in the EU have risen by almost 80 per cent since 2019, and scrap has been traded too, at roughly more than 90 per cent of the LME ingot price. At these levels, the economic margin for converting scrap into secondary ingot collapses, undermining the viability of EU remelters and refiners’ prices; this is translating into postponed investments, curtailed recycling capacity and plant closures.

AL Circle: FACE has called for “targeted measures” to retain scraps in Europe. Which approach would you advocate for that to be most effective?

Mario Conserva: In light of growing tensions in the aluminium scrap market, FACE is calling for the adoption of a decisive and structural trade measure at the EU level. A robust instrument is needed to address the current market imbalance, flanked by complementary measures such as targeted incentives, administrative simplification and improvements to the regulatory framework. FACE considers the introduction of a high export tariff on aluminium scrap to be an effective and proportionate solution to support Europe’s recycling and processing industry. A meaningful tariff would help stabilise domestic scrap prices at levels compatible with EU recycling economics, which are currently under pressure due to significant global price differentials. This would restore investment in advanced sorting and recycling technologies, key elements for strengthening an efficient and competitive circular value chain. By contrast, low or merely symbolic duties would not materially alter trade flows under current market conditions. If set at a level that genuinely shifts economic incentives, a high export tariff could be a balanced, enforceable and WTO-defensible solution to reinforce Europe’s industrial sovereignty in the aluminium sector.

AL Circle: Some industry voices support export tariffs on scrap, while others warn it may distort trade. Should the EU balance internal supply security in compliance with WTO rules and trade partners?

Mario Conserva: The market has segments that move along related but different paths, objectives and motivations; FACE is looking at the most significants needs of our typical market and we see mid mounting tensions in the aluminium scrap market, and to the most common interests of our people it is urging the European Union to adopt a decisive and structural trade measure to correct what it describes as a growing market imbalance. Such a measure should be accompanied by complementary actions, including targeted incentives, administrative simplification and improvements to the regulatory framework. The sector is currently under severe pressure due to significant global price differentials; by restoring more balanced price conditions, a strong tariff could in turn rebuild investment confidence in advanced sorting and recycling technologies — key pillars of a competitive and efficient circular value chain. FACE also highlights the flexibility of a price-based trade instrument: a high export tariff offers a balanced, enforceable and WTO-defensible solution, provided it is set at a level that genuinely changes economic incentives. Together with other European organisations in the aluminium segment and in collaboration with important industrial operators in the downstream segment, we are working with the Commission to optimise the classification criteria.

AL Circle: What is your advice to the policymakers for addressing the risk that Europe may become a scrap yard, while still meeting decarbonisation and circular economy goals?

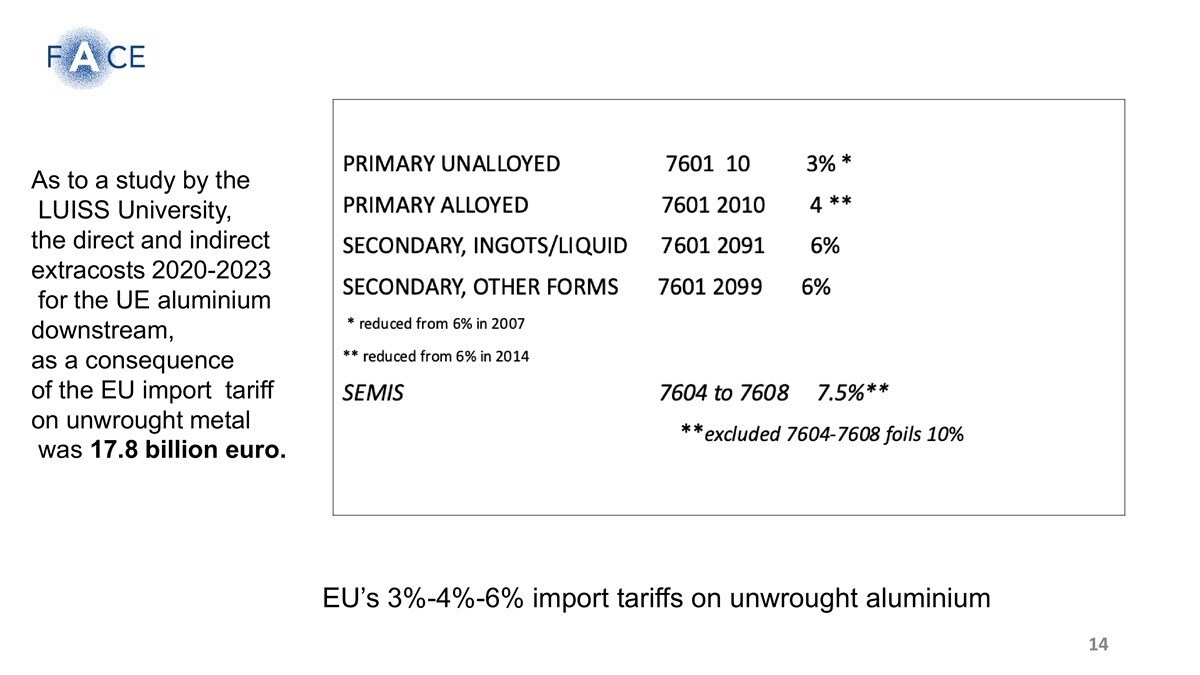

Mario Conserva: Our message to policymakers is clear: exporting aluminium scrap means exporting energy and a strategic raw material that Europe does not have in sufficient supply. This must be considered within the broader context of the European aluminium ecosystem, which is built on a long-standing industrial tradition, significant expertise, know-how and technological capability. At the same time, the challenges facing the sector must be acknowledged, and secondary aluminium production should be more and more encouraged through appropriate support schemes, other than customs duties. Anyhow, it is to remind that primary aluminium must be blended with recycled metal for most applications, so that even in the most ambitious circularity scenario, EU deficit and imports of primary metal will continue to grow. In addition, our industry is confronted with complex regulatory and administrative burdens, the highest energy costs globally, and a quite complex supply chain (Figure 12; Figure 13). Moreover, imports of primary aluminium in the EU remain subject to duties, which ultimately undermine the competitiveness of downstream European industry with artificial direct and indirect extra costs evaluated some years ago in a study by the University of LUISS for FACE, about the industrial aluminium system in Europe (Figure 14).

Against this backdrop, investments in recycling are and will increasingly remain a concrete reality and a strategic opportunity that must be managed in the most effective and forward-looking way possible.